The FX instrument suite. Five instruments. One market. Completely different obligations.

People often think FX is simply a question of locking an exchange rate. In reality, choosing the right instrument is usually more important than the rate itself.

Most FX products exist for a reason. Some solve settlement problems. Some solve funding problems. Some remove uncertainty completely. Others preserve flexibility when the exposure itself is uncertain. They all trade the same currencies, but they behave very differently.

Five parts of the FX toolkit worth understanding.

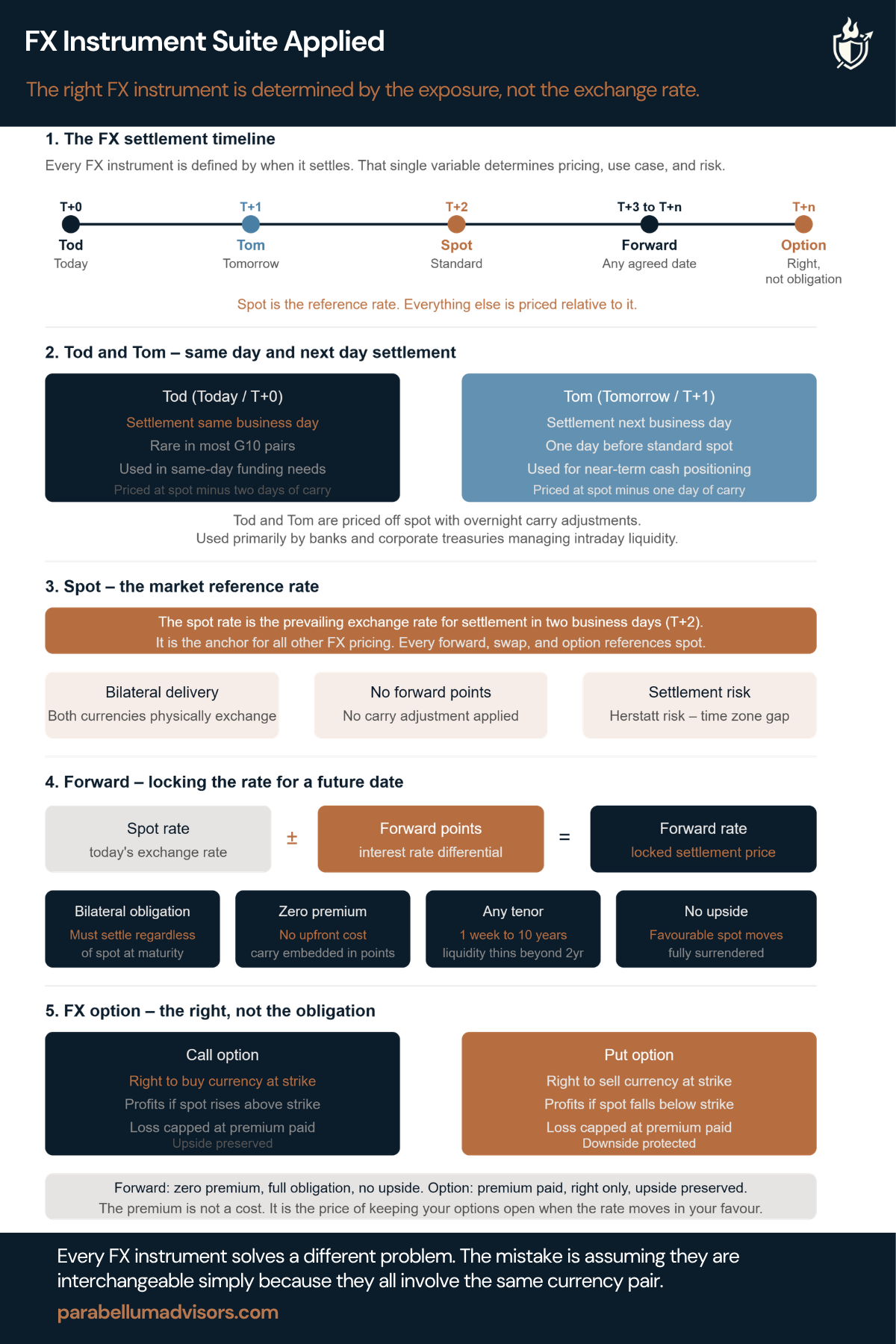

1. Settlement first

Every FX instrument begins with one question. When do the currencies actually need to change hands?

Tod settles today. Tom settles tomorrow. Spot generally settles two business days later. Beyond that, you move into forwards and options. Everything else, including pricing, is built from that settlement date.

2. Spot isn’t the beginning or the end

Spot is simply the market reference point. It is where every forward starts, where every FX swap is priced from, and where option strikes are measured against. It isn’t a forecast of where currencies are heading. It is simply today’s exchange rate for standard settlement.

3. Forwards remove uncertainty

When the exposure is known and the timing is fixed, an FX forward is usually the right answer. The rate is locked and both parties are committed to settle. That certainty is valuable, but it comes with a trade-off. If the market moves in your favour, you have already given that upside away.

4. Options preserve flexibility

Sometimes the exposure itself is uncertain. An acquisition may not complete. A project bid may not be successful. A contract may never be signed.

That is where an option earns its premium. You pay for the right to transact, not the obligation. If the exposure never materialises, neither does the hedge.

5. The instrument should match the exposure

Most hedging mistakes are not caused by using derivatives. They come from using the wrong derivative.

Using a forward when the transaction may never occur creates unnecessary obligations. Buying an option for a committed exposure may simply add unnecessary cost. Using spot funding when the real issue is liquidity can create avoidable operational risk.

The instrument should reflect the commercial reality, not simply the currency pair.

The FX market is full of sophisticated structures, but most problems are solved with a handful of well-understood instruments. The challenge is not learning how they work. It is knowing which one fits the problem you are actually trying to solve.

For treasury teams and investment managers, the question is usually less about where the exchange rate is going and more about whether the instrument you’ve chosen still behaves as expected if the underlying exposure changes.

FX Forwards Applied, FX Swaps Applied, Contingent FX Forwards Applied, Non-Deliverable Forwards Applied, Cross Currency Swaps Applied