Non-deliverable forwards. EM FX hedging looks like G10 FX hedging. It isn’t.

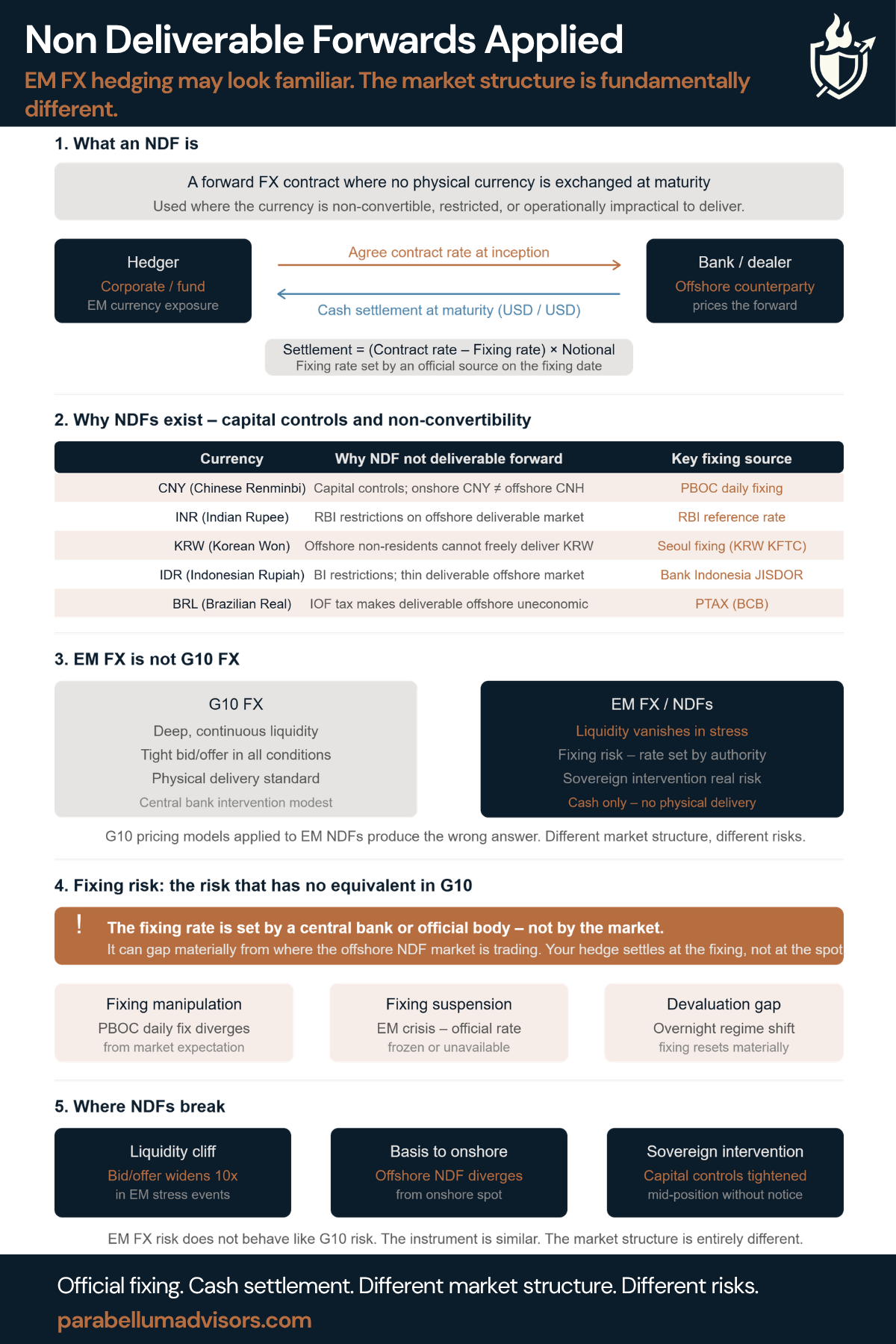

An NDF is a forward FX contract where no physical currency changes hands at maturity. You agree a rate today. At fixing, the difference between the contract rate and the official fixing rate is cash settled in USD.

The mechanics are simple. The market structure is not.

The traders who get caught in EM FX tend to apply G10 thinking to a market that simply does not work that way. The contract may look familiar. The liquidity, settlement process, regulatory environment and failure modes are fundamentally different.

Five things to understand about non-deliverable forwards.

1. What an NDF actually is

An NDF is a bilateral forward contract referencing a restricted or non-convertible currency. At inception the two parties agree a forward exchange rate exactly as they would for a deliverable forward.

The difference comes at maturity. No EM currency is exchanged. Instead, settlement is calculated as the difference between the agreed contract rate and the official fixing rate, multiplied by the notional and paid in USD. The economic exposure is preserved. The currency itself never leaves its domestic market.

2. Why NDFs exist -capital controls and non-convertibility

NDFs exist because the underlying currency cannot be freely delivered. Capital controls, convertibility restrictions, offshore access limits or punitive transaction taxes make physical delivery either illegal, impractical or uneconomic for offshore participants.

3. EM FX is structurally different from G10 FX

This is the most important point to understand before trading a single NDF.

In G10 markets you expect deep liquidity, relatively stable bid-offer spreads, continuous price discovery and physical delivery. EM markets behave differently.

Liquidity can disappear within hours during stress events. Bid-offer spreads can widen dramatically. Sovereign intervention can arrive without warning. Settlement occurs against an official fixing that may diverge materially from where the offshore market has been trading.

4. Fixing risk

In a deliverable G10 forward, settlement occurs against the prevailing market exchange rate. An NDF settles against an official fixing published by the relevant authority. That single distinction changes the entire risk profile; settlement is determined by an official benchmark rather than continuous offshore trading.

5. Where NDF programmes break

Liquidity – The hedge that was straightforward to execute can become expensive or impossible to adjust as market depth disappears and bid-offer spreads widen.

Basis – The relationship between the offshore NDF market and the onshore spot market can diverge materially during periods of stress, leaving the hedge settling against a rate that no longer reflects the underlying exposure.

Sovereign intervention – Capital controls can change. Offshore access can tighten. Fixing methodologies can evolve.