FX swaps. The instrument every treasurer uses and almost nobody fully prices.

An FX swap is two legs (the near leg and the far leg). You sell a currency at spot today and buy it back at a predetermined forward rate on a fixed date. Simple in execution. Not simple in risk.

Five things you need to understand before you roll another FX swap book.

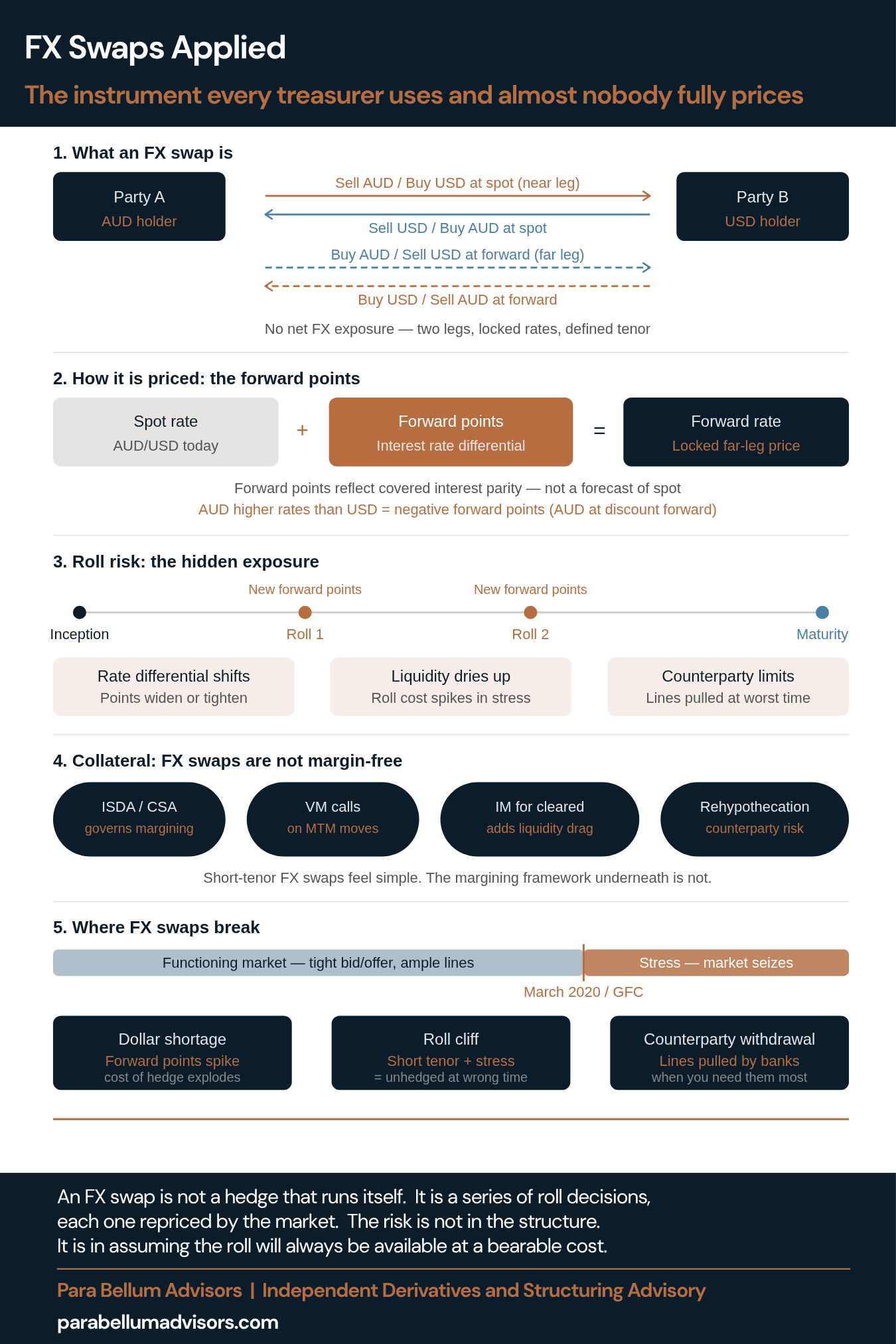

1. What it is

Two simultaneous transactions. Near leg: exchange currencies at today’s spot rate. Far leg: reverse the exchange at a pre-agreed forward rate. No net FX exposure on the principal – both rates are locked at inception. What changes is the cost of carry embedded in those forward points.

2. How it is priced

Forward points are driven by the interest rate differential between the two currencies, not by anyone’s view on where spot is going. If AUD rates are higher than USD rates, AUD trades at a forward discount. You pay that differential to hold the hedge. This is covered interest parity. It is not negotiable. What is negotiable is the bid/offer spread, and that matters more than most treasuries realise.

3. Roll risk: the exposure that builds slowly and continuously

Most FX swaps are short-dated – one week to three months. That means the hedge is not a set-and-forget. It is a rolling programme. Each time you roll, you reprice at whatever the forward points are on that day. If rate differentials have moved, your hedging cost has moved. If the market is stressed, your cost has moved sharply. The roll cliff – when a large notional comes due in a dysfunctional market –is where FX swap programmes genuinely fail.

4. Collateral: not as simple as it looks

FX swaps sit under ISDA agreements with CSA margining. Variation margin moves with MTM. For cleared trades, initial margin adds a standing liquidity drag. The rehypothecation of posted collateral introduces counterparty credit exposure that sits quietly in the background until it doesn’t. Short tenor does not mean zero operational complexity.

5. Where it breaks

Dollar shortage events – GFC, March 2020 – push forward points to levels that make hedging economically irrational. Bank counterparties pull lines precisely when notional volumes are highest and alternatives are fewest. A programme built on the assumption of continuous market access is not a hedged programme. It is a programme that works until it doesn’t.

FX swaps are the right tool for managing short-dated currency exposure. The structure is sound. The risk is in treating the roll as automatic and the cost as fixed.