FX forwards. They remove uncertainty. They also remove flexibility.

An FX forward is probably the most widely used derivative in corporate treasury. Agree an exchange rate today, settle at a future date, and the currency risk disappears.

For committed exposures, it is a remarkably effective instrument.

The problems usually begin when the underlying exposure changes rather than the exchange rate.

Five things corporate treasurers and fund managers should understand about FX forwards.

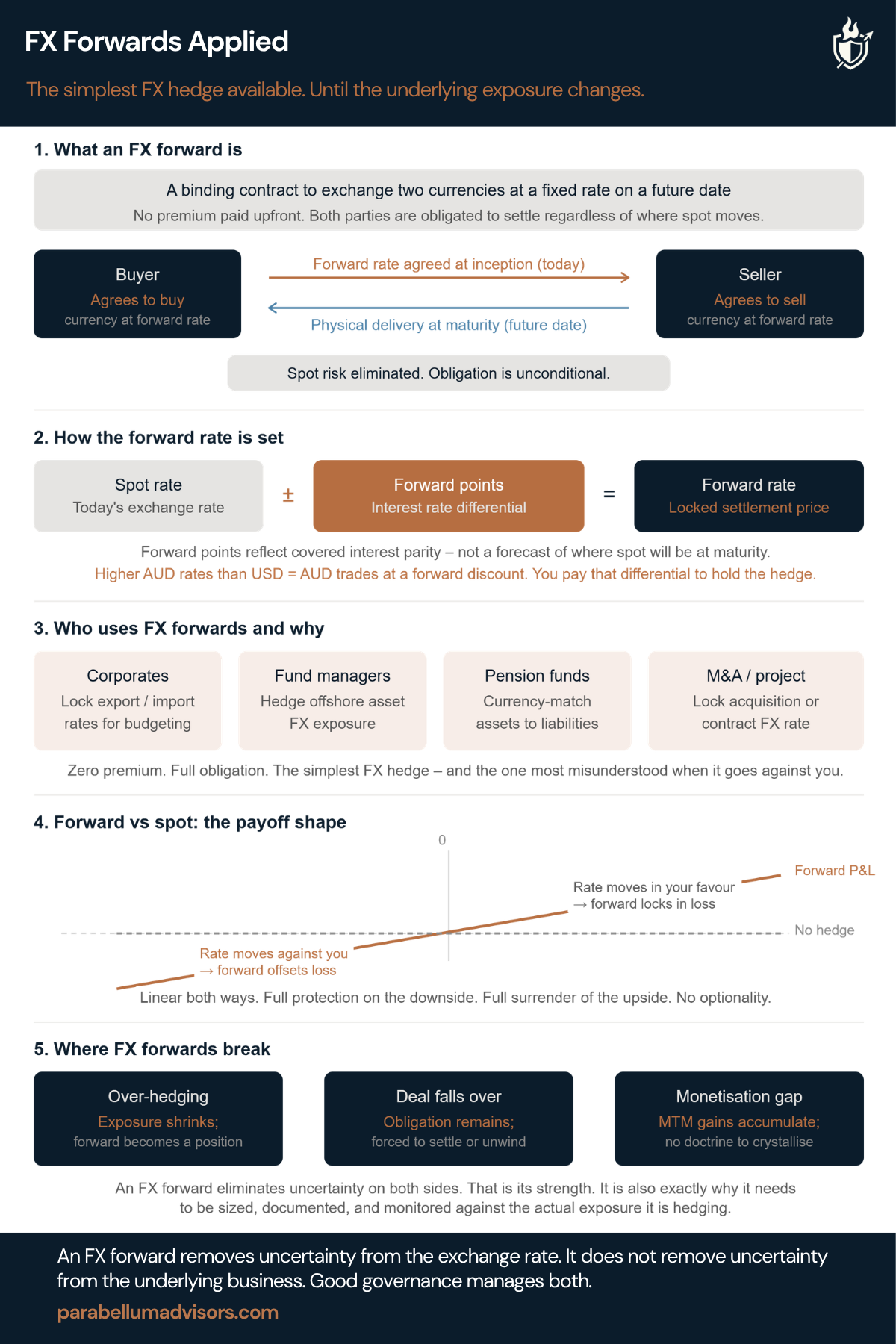

1. What an FX forward actually does

An FX forward locks the exchange rate today for a future transaction. There is no upfront premium and no optionality. Both parties are committed to exchange the agreed currencies on the settlement date, regardless of where the spot market has moved.

2. The forward rate is not a market forecast

One of the most common misconceptions is that the forward tells you where the market expects the exchange rate to trade. It does not. The forward rate is simply today’s spot rate adjusted for the interest-rate differential between the two currencies. The market may ultimately settle above or below that level. The forward is pricing financing, not predicting direction.

3. Why institutions use them

The attraction is certainty. Exporters lock future revenues. Importers lock future costs. Asset managers hedge offshore investments. Pension funds align foreign assets with domestic liabilities. The objective is rarely to generate returns. It is to remove currency as a source of uncertainty.

4. The hedge and the exposure should always be viewed together

An FX forward should never be judged in isolation. If the forward loses money, the underlying exposure should be benefiting by roughly the same amount, and vice versa. Looking only at the derivative P&L is one of the quickest ways to conclude that a successful hedge has somehow failed.

5. Where programmes usually break

The instrument is simple. The governance is often not. Exposures change, transactions are delayed and acquisitions fall over. The forward remains in place unless someone actively changes it. That is how a hedge quietly becomes a speculative position. Another common failure is never crystallising gains when a forward moves materially in the institution’s favour. The mark-to-market looks reassuring in the monthly report until the exchange rate reverses and the opportunity disappears.

FX forwards remain the workhorse of corporate FX risk management for a reason. They are straightforward, transparent and effective.

The important question is not whether the hedge worked. It is whether the exposure it was protecting is still the same as the day the trade was executed.

FX Swaps Applied, Cross Currency Swaps Applied, Non-Deliverable Forwards Applied, FX Overlays That Behave