By Mike Duncan | January 2026

When floating funding turns growth into a survival problem.

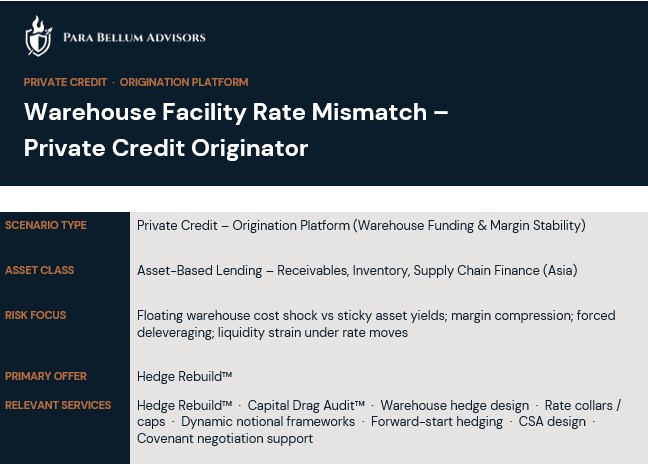

Sector: Private Credit – Origination Platforms

Asset Class: Asset-Based Lending (Receivables / Inventory / Supply Chain Finance – Asia)

Situation Type: Warehouse-funded lending with sticky asset pricing

Primary Issue: Margin compression, covenant pressure, and forced deleveraging driven by funding mechanics, not credit stress

The Situation

Private credit originators frequently rely on warehouse facilities with floating-rate funding while originating assets priced on fixed or slow-reset terms.

On paper, the platform appears to be short-duration.

In reality, it carries structural exposure to rapid funding repricing, amplified by high utilisation and committed origination pipelines.

When base rates move sharply, funding costs reprice immediately while asset yields lag – often by quarters.

Why This Scenario is Common

Warehouse facilities are treated as operational infrastructure, not as risk positions.

As platforms scale, funding volatility becomes a first-order driver of outcomes – but remains unmanaged until damage shows up in reported performance.

By then, optionality is already gone.

Why It Matters

Margin compression accelerates faster than governance can respond.

Even with stable credit performance:

-

ROE collapses

-

Covenants tighten mechanically

-

Repricing becomes commercially and politically difficult

-

Growth decisions turn into defensive liquidity management

The platform doesn’t fail because of losses. It fails because funding convexity was never bounded.

How This Is Typically Addressed

Rather than attempting to “time rates” or fully lock funding:

-

Funding risk is explicitly bounded rather than eliminated

- Hedge notionals are aligned dynamically to utilisation, not commitments

- Protection is designed around margin survival, not accounting optics

- Governance thresholds are embedded, so decisions occur before stress

The objective is to preserve control – not to predict markets.

Primary Engagement Route

Hedge Rebuild™ – Funding and margin risk redesign across warehouse utilisation, hedging, liquidity, and governance

Full structural narrative shared selectively on request.

Illustrative scenario for discussion purposes only. Not a transaction summary or client-specific case study.