Tail hedges. Diversification fails when you need it most. Convexity doesn’t.

Institutional portfolios are built on diversification. Equities, bonds, credit and alternatives. The assumption is straightforward: when one asset class struggles, another should provide stability. History suggests otherwise.

In every major market dislocation of the past three decades, correlations have moved sharply higher, liquidity has deteriorated and diversification has delivered far less protection than expected. Diversification is not flawed. It was never designed to protect against extreme market stress.

That is the role of convexity.

Five things every CIO and investment committee should understand about tail hedging.

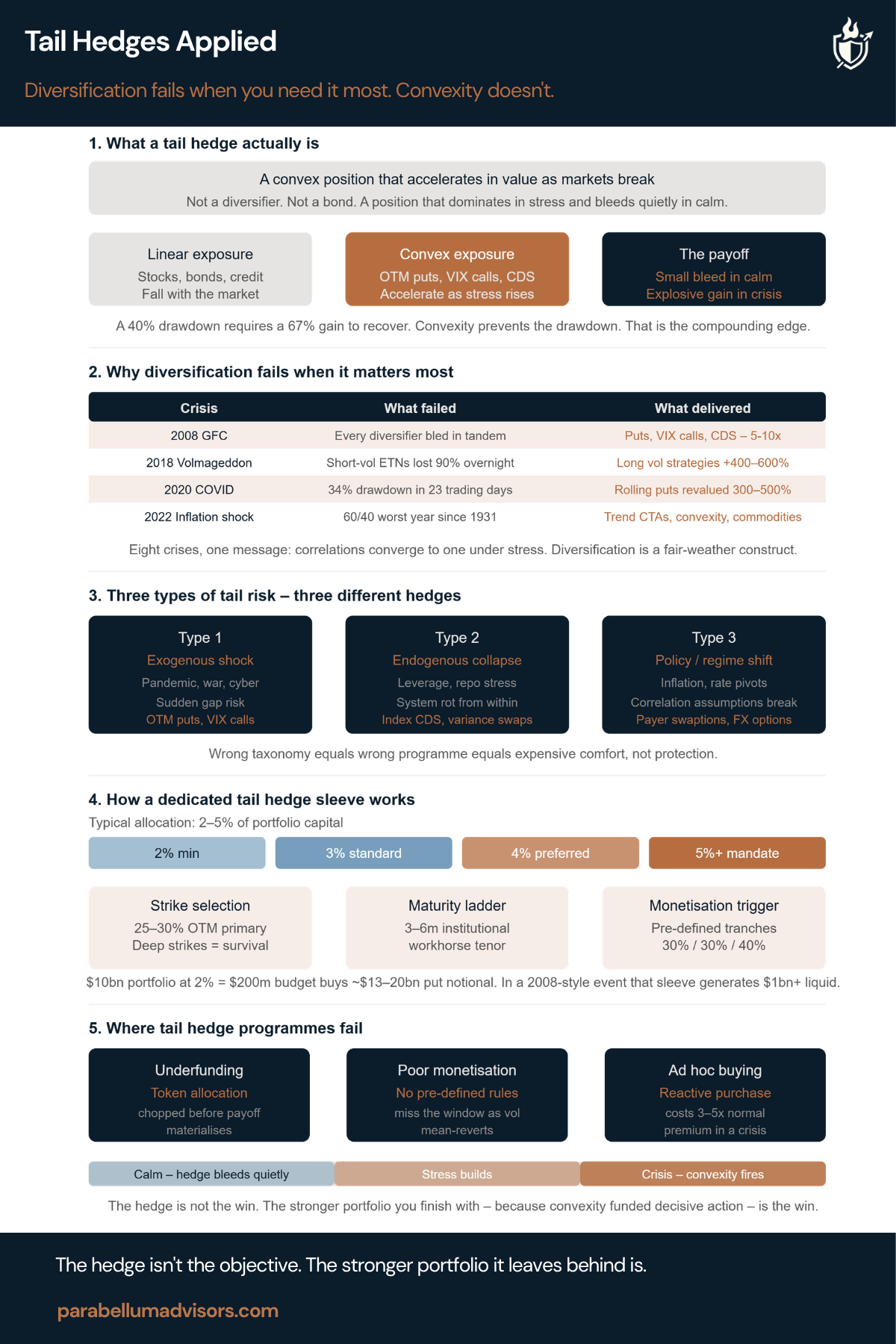

1. What a tail hedge actually is

A tail hedge is not another diversifier. It is a deliberately convex position designed to accelerate in value as markets deteriorate. A conventional asset allocation seeks to reduce volatility. A tail hedge creates liquidity precisely when the rest of the portfolio is under maximum pressure.

A 40% drawdown requires a 67% recovery. Preventing the drawdown is far more valuable than recovering from it.

2. Why diversification runs out of road

The GFC, COVID and the 2022 inflation shock all looked different. Portfolio behaviour was remarkably similar. Correlations increased, liquidity disappeared and assets expected to diversify each other began moving together.

Diversification remains the first line of defence. Convexity is one of the few protections that does not depend on correlations remaining low.

3. Different tails require different protection

Not every crisis looks the same. Equity crashes, credit events, inflation shocks and currency dislocations require different forms of protection.

The objective is not to own more hedges. It is to own the right convexity for the risks embedded in the portfolio.

4. Governance matters more than sophistication

The design of most institutional tail hedge programmes is rarely the problem. Governance usually is. Markets can reprice in days. Investment committees often meet monthly.

Without delegated authority and pre-defined monetisation rules, even a well-designed programme can fail when it matters most.

5. Where programmes fail

Most failures are predictable. Protection is bought after volatility has repriced. Premium budgets are cut because the programme appears to underperform in calm markets.

Convexity gains are never monetised because committees wait for certainty.

The institutions that compound successfully across decades are rarely those with the most sophisticated hedges. They are the ones with the discipline to maintain them, the governance to act decisively and the liquidity to improve the portfolio when others cannot.

Tail hedging is not about predicting crises. It is about ensuring your portfolio has both the resilience to survive and the liquidity to take advantage of the opportunities a crisis creates.