An IRS locks the rate. A swaption locks the decision.

A swaption gives you the right, not the obligation, to enter an interest rate swap at a predetermined fixed rate. You pay a premium upfront. If rates move against you, you exercise. If they do not, you walk away. That asymmetry is why a swaption is not simply an expensive IRS.

Five things to understand about swaptions.

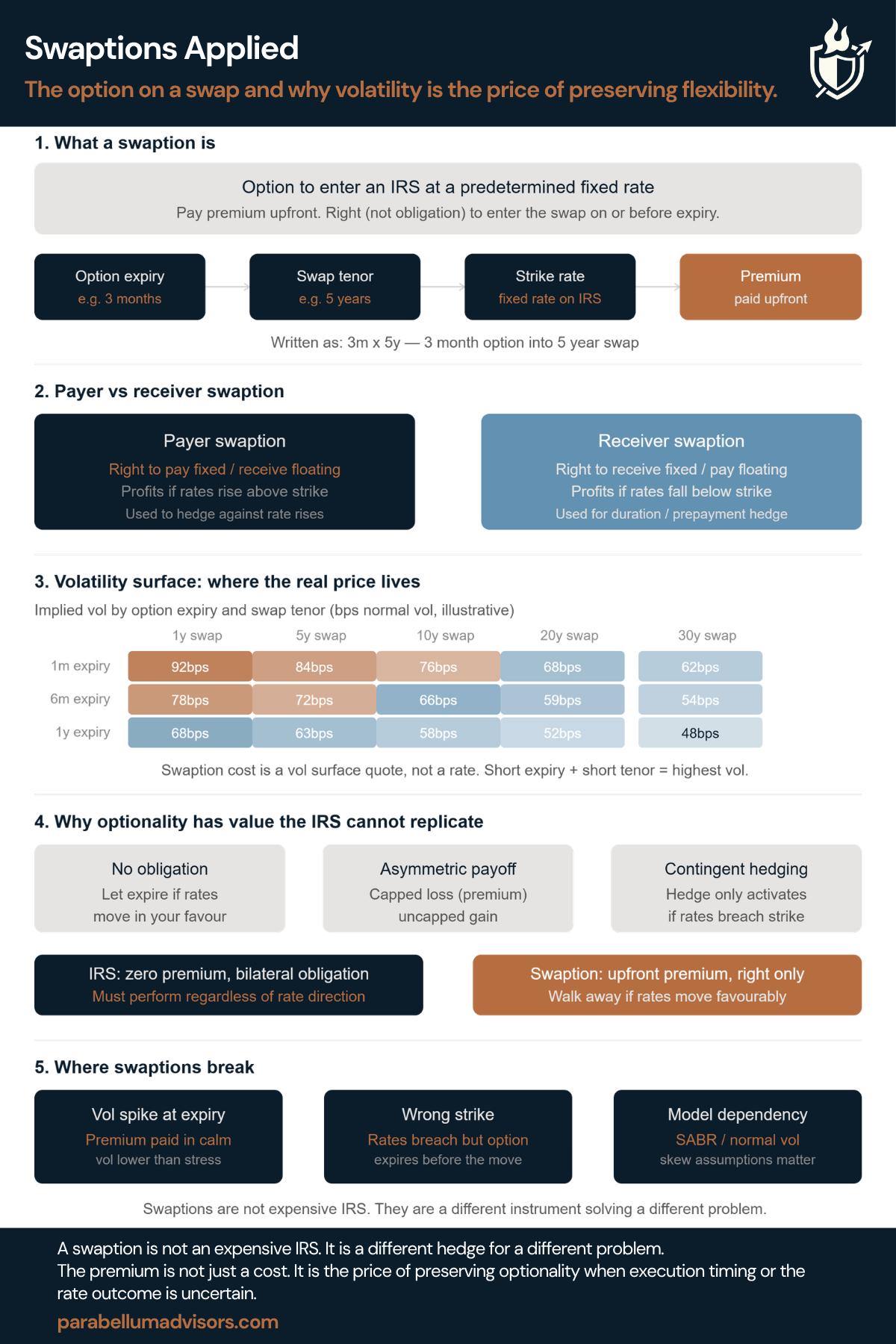

1. What a swaption is

An option to enter an IRS at a fixed strike rate, with a defined expiry and an underlying swap tenor. Written as expiry x tenor. A 3m x 5y is a three-month option to enter a five-year swap. The buyer pays premium at inception and decides at expiry whether to exercise based on where the market rate sits relative to the strike.

2. Payer vs receiver

A payer swaption gives you the right to pay fixed and receive floating. It benefits if rates rise above the strike. Used by corporates hedging floating-rate debt, or by funds managing duration extension risk. A receiver swaption gives you the right to receive fixed and pay floating. It benefits if rates fall below the strike. Used for liability-matching, mortgage prepayment hedging, and duration management by insurers and pension funds.

3. The vol surface: where the real price lives

A swaption is not priced off the rate curve alone. It is priced off a volatility surface: implied volatility by option expiry and underlying swap tenor. When you receive a swaption premium quote, you are looking at a point on that surface. The question is whether the implied volatility is fair for the risk being transferred.

4. What optionality gives you that an IRS cannot

An IRS is a bilateral obligation. Once you are in it, you are in it. A swaption preserves the upside. If rates fall sharply, or if the underlying transaction changes, you let the option expire and access the lower rate in the market. The premium is the cost of retaining that choice. For mandates where the rate exposure is genuinely uncertain, such as pre-deal hedging, contingent refinancing, and M&A rate locks, the swaption is often the cleaner instrument.

5. Where swaptions break

Expiry matters. If the option expires before the rate risk crystallises, the hedge disappears before it is needed. Strike selection matters. A 50 basis point out-of-the-money strike can look cheap until the market moves 45 basis points. Model dependency also matters. Assumptions around the vol surface and skew can materially change the premium for the same notional and tenor.

Swaptions are not expensive interest rate swaps. They solve a different problem.