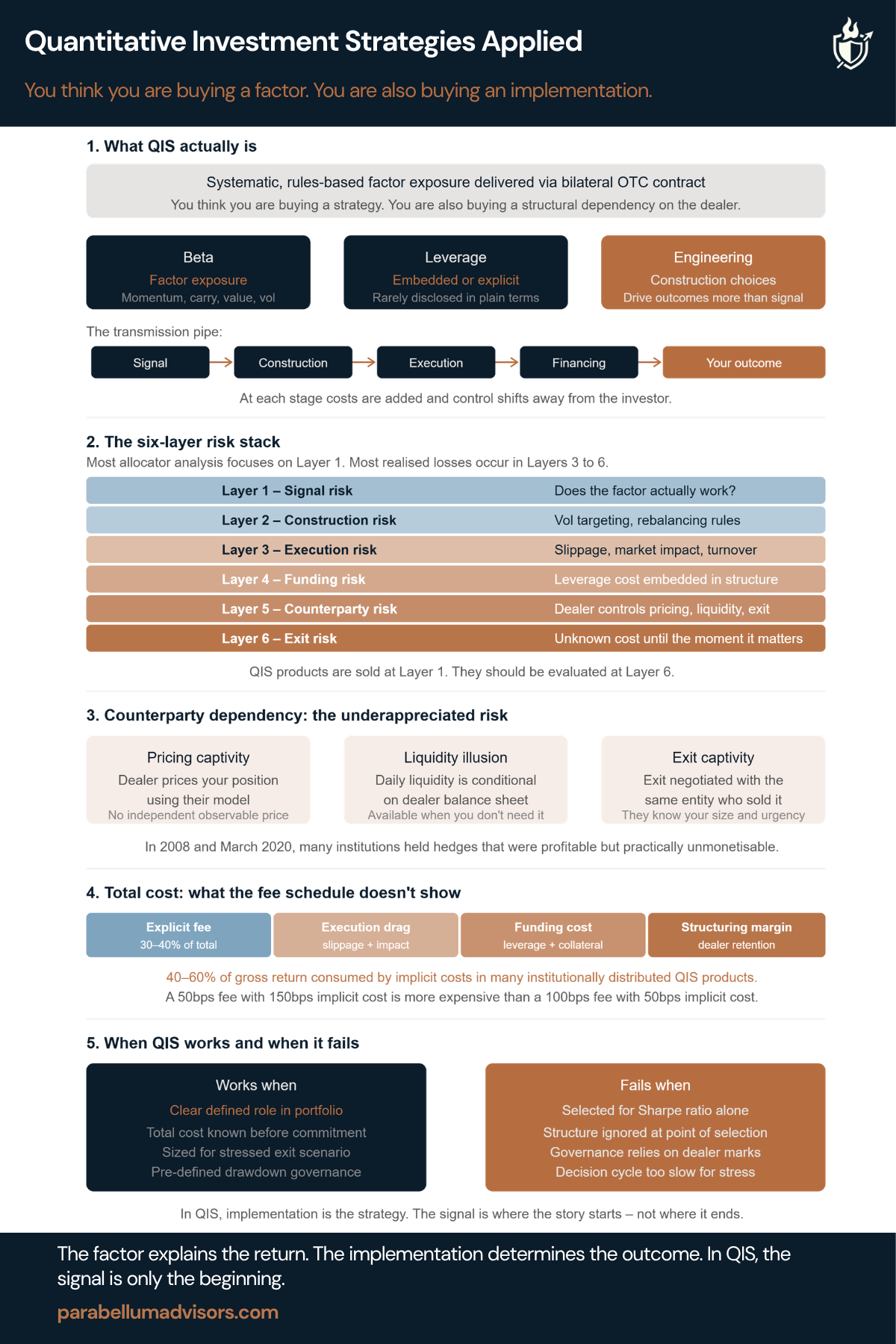

You think you are buying a strategy. You are also buying a structural dependency on the dealer.

QIS is sold as systematic, diversified, transparent and efficient. None of that is wrong. It is simply incomplete.

Most allocators believe they are buying exposure to a factor such as momentum, carry, value or quality. In reality they are also buying a construction methodology, a financing model, an execution framework and a dealer relationship. The factor explains part of the return. Everything wrapped around it often determines the outcome.

Five things every institutional investor and investment committee should understand about QIS.

1. What QIS actually is

At its core, a QIS is a rules-based strategy designed to capture a recognised source of return. The underlying signal is usually well understood. What matters just as much is how that signal is translated into a live portfolio through leverage, rebalancing, execution and derivative implementation.

Those engineering decisions frequently matter more than the factor itself.

2. There is more than one source of risk

Most due diligence focuses on whether the factor works. That is only the first layer.

Construction, execution, funding, counterparty exposure and exit mechanics all influence realised outcomes. The strategy may perform exactly as designed while the implementation disappoints. Understanding the wrapper is often more important than understanding the signal.

3. Counterparty dependency is part of the investment

Most QIS strategies are delivered through bilateral OTC structures. That means the dealer often provides the pricing, execution, financing and liquidity. The factor may be systematic. The implementation is not.

A portfolio that appears diversified by factor can still be highly concentrated through its dependence on a single dealer.

4. The fee is rarely the total cost

The headline management fee is usually the smallest component.

Execution costs, financing, collateral, turnover and dealer structuring margins all affect realised returns. The relevant comparison is never the fee schedule. It is the all-in implementation cost against the expected gross return of the strategy.

5. Where QIS succeeds and where it fails

QIS works best when it has a clearly defined role within the portfolio, realistic return expectations and governance that recognises implementation risk as well as factor risk.

It fails when the investment decision stops at the backtest, costs are underestimated and the dealer wrapper receives less scrutiny than the underlying signal.

In QIS, implementation is the strategy. Two institutions can buy exposure to the same factor and experience very different outcomes. The difference is rarely the signal. It is the structure built around it.