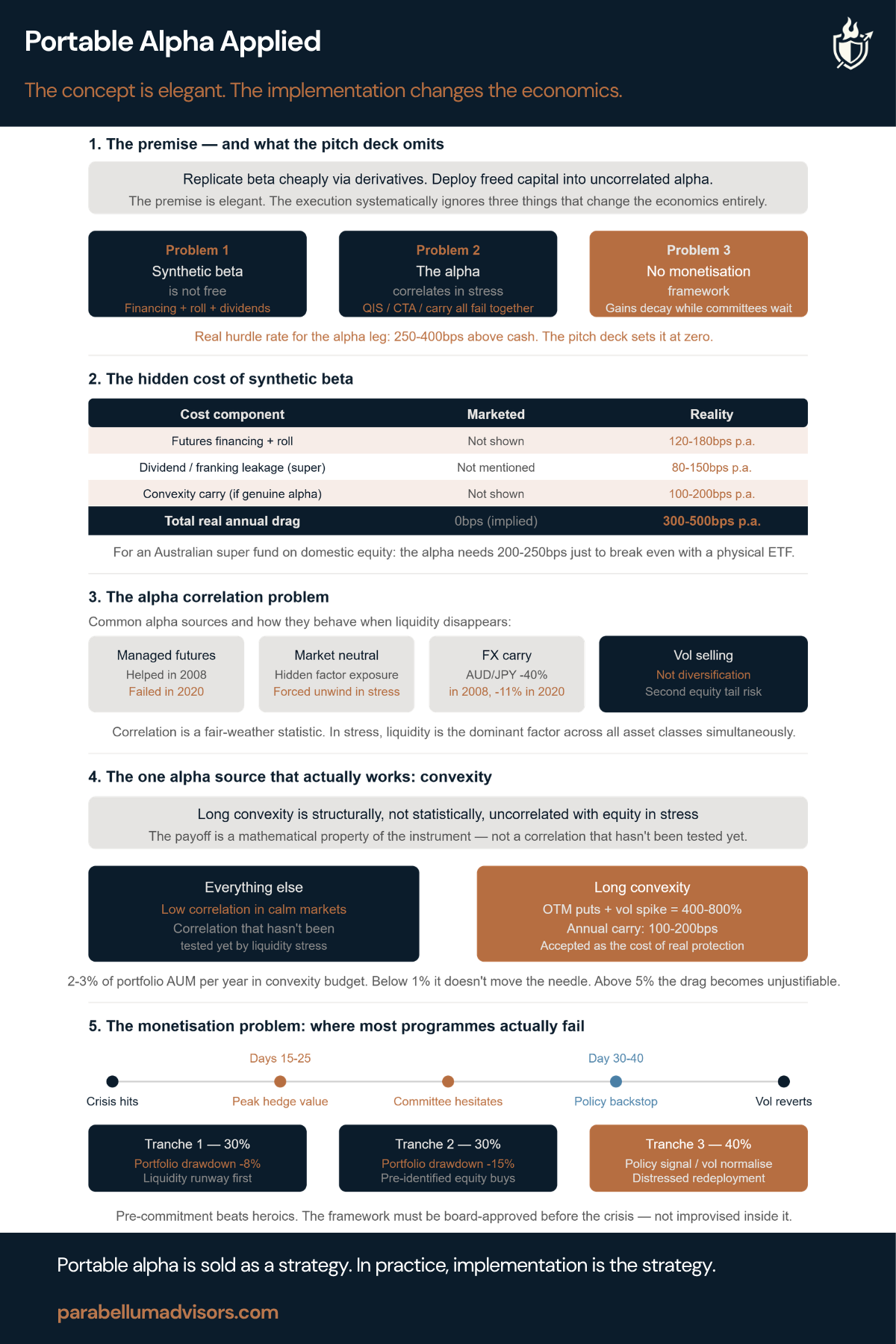

The premise is elegant. The execution systematically ignores three things that change the economics entirely.

Portable alpha has an appealing logic. Separate beta from alpha. Replicate the market cheaply using derivatives. Invest the remaining capital into genuinely independent sources of return.

If everything works, the portfolio earns market beta plus alpha, with less drawdown because the alpha behaves differently when markets come under stress. The concept is sound. The implementation often isn’t.

Most portable alpha structures fail for the same three reasons. The cost of synthetic beta is understated. The alpha proves less independent than expected when markets become stressed. No one has decided how gains will be monetised if the programme works.

Five things every CIO, allocator and investment committee should understand.

1. The concept is elegant. The implementation is where the economics change

Portable alpha is often presented as though separating beta from alpha is almost costless. It isn’t.

Every implementation introduces financing costs, roll costs, collateral requirements and execution decisions that materially affect realised returns. The strategy should never be assessed without pricing those costs honestly.

2. Synthetic beta isn’t free

Derivative beta always carries an economic cost. Financing, futures roll, collateral and, for Australian investors, the loss of franking credits all raise the hurdle the alpha sleeve must overcome before the structure creates any additional value.

The relevant question is never whether the alpha works. It is whether the alpha exceeds the true cost of carrying the synthetic beta.

3. Most alpha isn’t as independent as the backtest suggests

Many portable alpha programmes rely on strategies that appear uncorrelated during normal markets. That is not the same as being structurally uncorrelated during market stress.

Carry, market-neutral equity, managed futures and many QIS strategies all have periods where liquidity becomes the dominant risk factor and correlations rise together. The distinction between statistical diversification and structural diversification matters far more than most pitch decks show.

4. Convexity is different

Long convexity is one of the few return sources that becomes more valuable because markets are breaking. Its behaviour is driven by the mathematics of the instrument rather than historical correlation.

That makes it fundamentally different from most portable alpha sleeves built around alternative risk premia.

5. The programme still has to be monetised

Even a well-designed portable alpha programme can fail if no one has authority to realise gains. The best structures define monetisation triggers before markets become stressed, not afterwards.

Implementation doesn’t stop when the hedge is established. It ends when the liquidity created by the programme has been converted into a stronger portfolio.