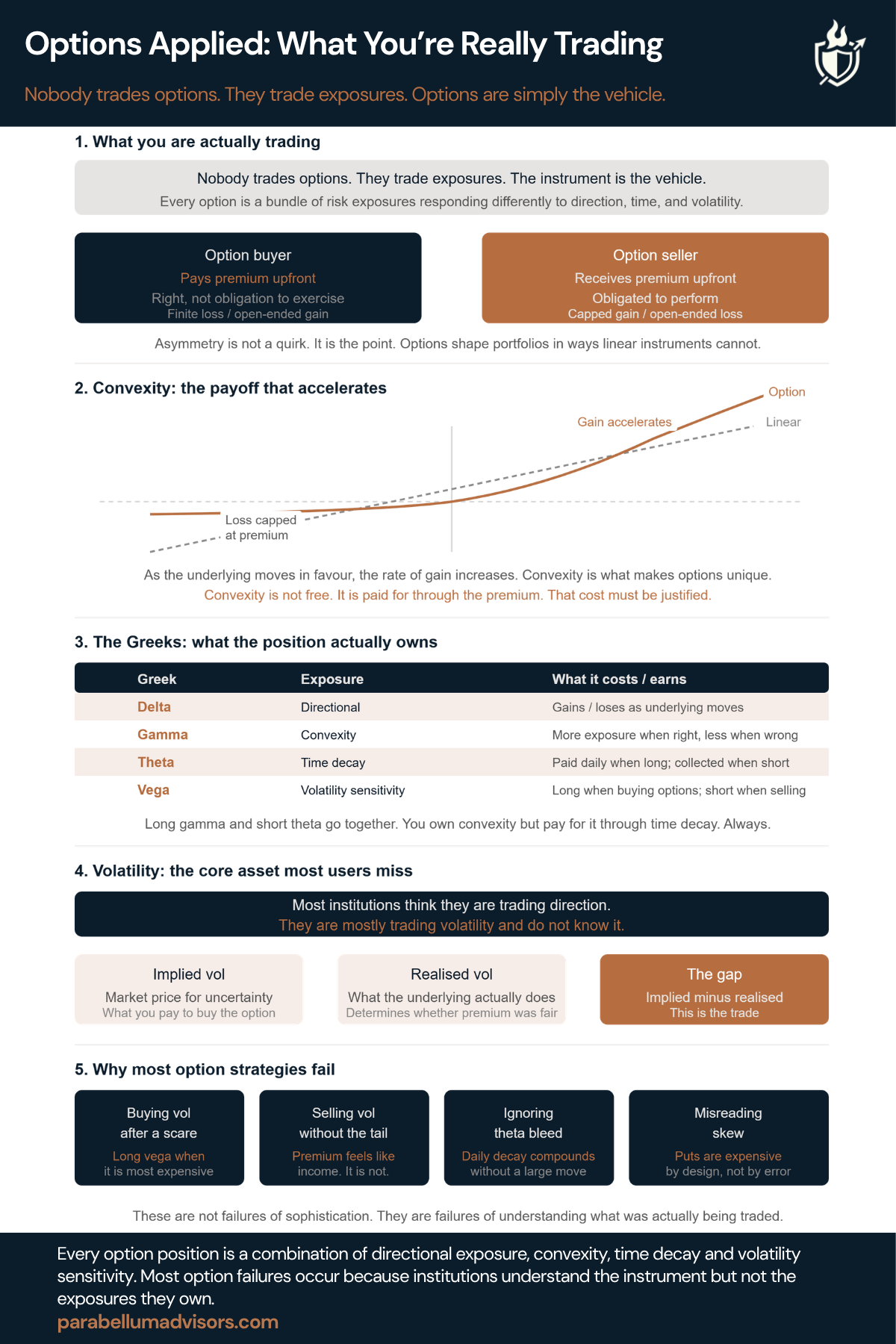

Options. Nobody trades options. They trade exposures. The instrument is the vehicle.

Most institutions that use options believe they understand them. They can describe a call. They know puts provide protection. What they often do not understand is what they are actually trading.

An option is not simply a bet on direction. It is a bundle of risk exposures. When you buy one, you are simultaneously taking positions on direction, volatility, convexity and time. When you sell one, you reverse those exposures.

That reframe changes everything.

Five things to understand about options.

1. What you are really trading

Trading desks do not think in terms of calls and puts. They think in terms of exposures.

- Long gamma.

- Short vega.

- Theta bleed.

- Rich or cheap implied volatility.

The instrument is secondary. The exposure is primary.

2. Convexity

Options are non-linear instruments. As markets move in your favour, gains can accelerate. As they move against you, losses are limited to the premium paid.

That asymmetry is convexity, and it is one of the most valuable characteristics options introduce into a portfolio. It is never free.

3. The Greeks

Every option position is a package of measurable exposures.

- Delta measures directional risk.

- Gamma measures convexity.

- Theta is the cost of owning convexity through time.

- Vega measures sensitivity to changes in implied volatility.

Understanding the Greeks means understanding what the portfolio actually owns.

4. Volatility

Most institutions think they are trading direction. They are mostly trading volatility.

The key distinction is between implied volatility, which the market prices today, and realised volatility, which the market ultimately delivers. That gap is where much of the economics of every option trade sits.

5. Why option strategies fail

The failure modes are remarkably consistent.

- Buying protection after implied volatility has already spiked.

- Selling volatility without recognising the tail risk being assumed.

- Ignoring the cumulative cost of theta.

- Treating downside skew as a pricing anomaly rather than a structural feature of the market.

Options are not strategies. They are risk tools that reshape portfolio exposures. Success comes from understanding those exposures before entering the trade, not after.

If you had to identify the single Greek driving your largest option position today, could you?