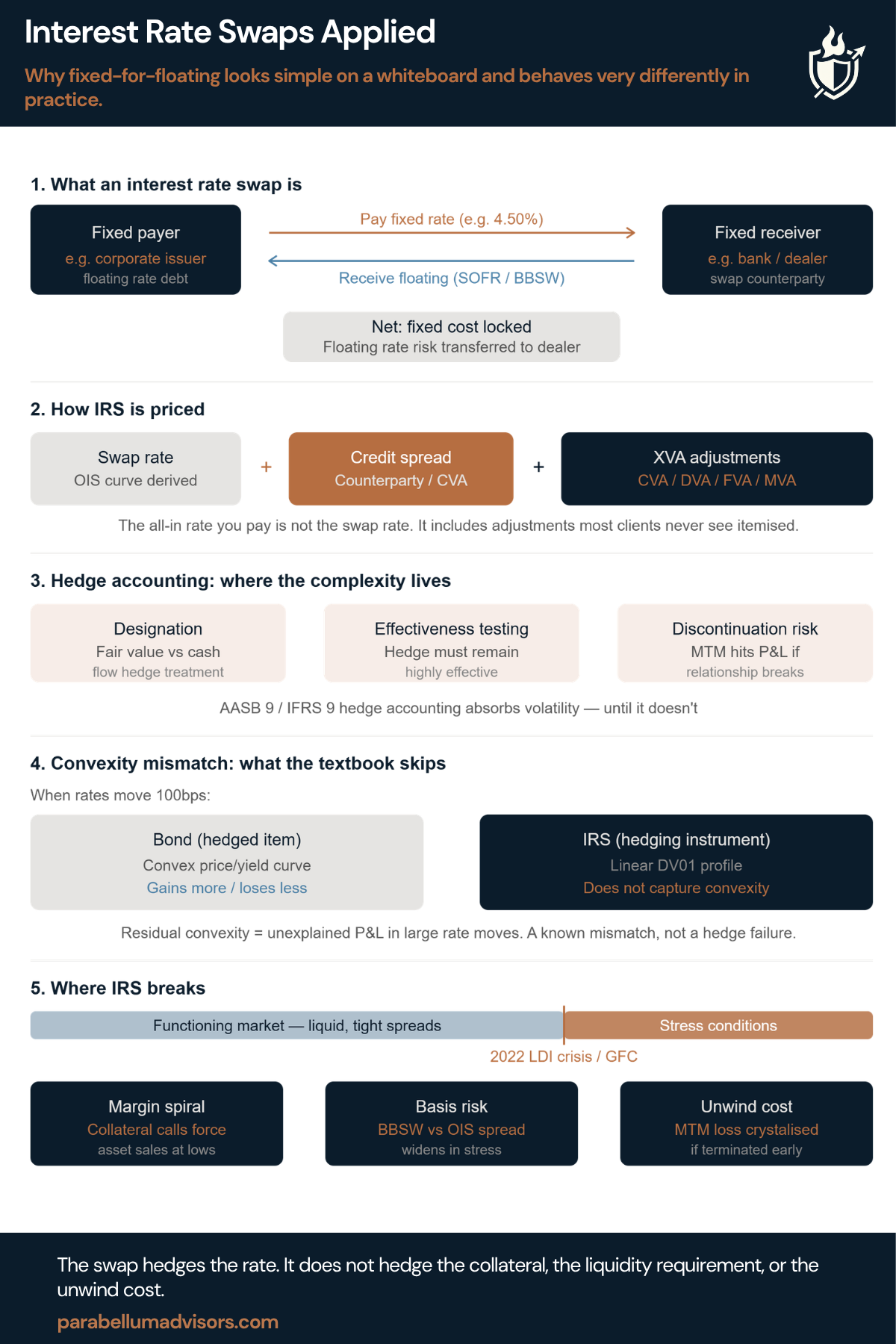

Most interest rate swap problems have nothing to do with interest rates.

You pay a fixed rate. You receive a floating rate. The net result is a locked rate exposure on the hedged debt. Clean on a whiteboard. Less clean when rates move 200bps in a quarter and your margin desk calls at 7am.

Five things people misunderstand about interest rate swaps.

1. An IRS doesn’t exchange principal

A bilateral agreement to exchange interest payments on a notional principal. No principal changes hands. The fixed payer locks in a rate and receives whatever the floating benchmark, SOFR or BBSW, prints each period. Used by corporates to convert floating-rate debt to fixed, by fund managers to manage duration, and by banks to manage structural balance sheet risk.

2. The quoted rate isn’t the whole economics

The quoted rate reflects the market curve together with funding, credit and capital adjustments, the XVA stack. Most clients negotiate the rate, not the economics underneath it.

3. Hedge accounting isn’t automatic

Under AASB 9 and IFRS 9, an IRS designated as a hedging instrument can defer MTM volatility into OCI rather than through P&L. That requires formal designation at inception, ongoing effectiveness testing, and documentation of the hedged risk. If the hedge relationship breaks because the underlying changes or the effectiveness test fails, accumulated MTM volatility may move through P&L.

4. A swap doesn’t hedge every interest-rate risk

An IRS converts floating interest into fixed interest. It does not hedge refinancing risk, credit spread movements, covenant changes or funding liquidity. Many boards assume “interest rate risk” has disappeared. It hasn’t. Only one component has.

5. Where IRS breaks

The 2022 UK LDI crisis. Pension funds using leveraged IRS portfolios for liability matching faced margin calls as rates rose sharply. To meet collateral, they sold gilts. Gilt sales pushed yields higher. Higher yields triggered more margin calls. The feedback loop required Bank of England intervention. The IRS worked as designed. The system around it did not.

An IRS is a precision instrument for managing rate risk. The risks are in the plumbing: margin mechanics, basis between the floating leg and your actual funding rate, and the cost of unwinding a deep out-of-the-money position before maturity.

Interest rate swaps look clean on a whiteboard. The real risk sits in margin mechanics, hedge accounting and basis – not the rate itself.