Equity total return swaps. Own the upside. Skip the balance sheet. Just know what you are paying for the privilege.

An equity total return swap gives an investor the economic return on a stock, basket or index without owning the underlying shares. No custody, no settlement and no legal title. For many institutional investors it is an efficient way to gain exposure while preserving balance sheet flexibility.

The attraction is obvious. The financing is often less so.

Most investors focus on the equity return. Over time, it is usually the funding spread that determines whether the programme delivers the economics originally expected.

Five things hedge funds, asset managers and institutional investors should understand about equity TRS.

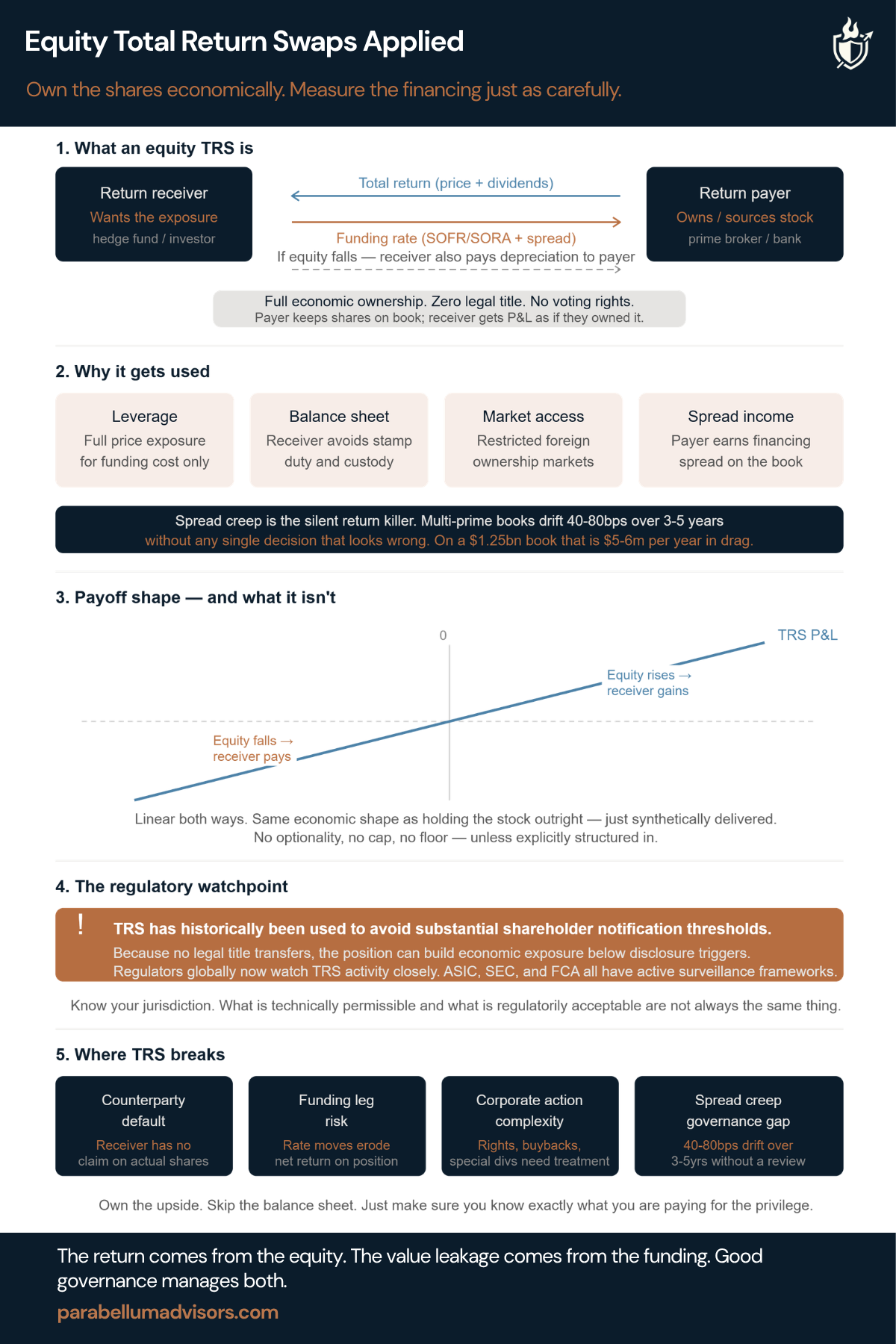

1. What an equity TRS actually is

An equity TRS transfers the economic return of an asset without transferring ownership. The investor receives the total return, including price movements and dividends, while paying a floating funding rate plus an agreed spread. If the shares rise, the investor benefits. If they fall, the investor bears the loss. Economically it behaves much like owning the stock outright. The difference is how that exposure is delivered.

2. Why it gets used

The structure provides efficient market access without requiring full cash outlay or direct ownership. It can improve capital efficiency, reduce operational complexity and simplify access to markets where holding physical shares is more difficult. For prime brokers, it creates an ongoing financing relationship rather than simply an execution relationship.

3. The economics go well beyond the equity return

An equity TRS is not simply a view on the underlying shares. It is also a financing decision. The funding spread is paid regardless of whether the investment performs well or poorly. As interest rates rise, or spreads widen over successive renewals, that cost quietly compounds. The equity may outperform while the financing steadily erodes the excess return.

4. Counterparty risk is part of the investment

The investor owns the economics, not the shares. That makes the relationship with the dealer important throughout the life of the trade. Pricing, collateral, corporate actions and the ability to exit all depend on the counterparty. A portfolio diversified across hundreds of companies can still be concentrated through a handful of prime brokers.

5. Where programmes usually fail

The biggest losses are rarely caused by the swap itself. They come from governance. Financing spreads drift higher over time, particularly in multi-prime relationships where renewals occur with little external benchmarking. Each increase appears reasonable in isolation. Over several years the programme can move materially away from market pricing without anyone making a single poor decision.

Equity TRS remains one of the most effective tools for gaining synthetic equity exposure. The structure is well understood and, for many investors, entirely appropriate.

The question is not whether the instrument works. It is whether the financing programme is still as competitive today as it was when the first trade was executed.