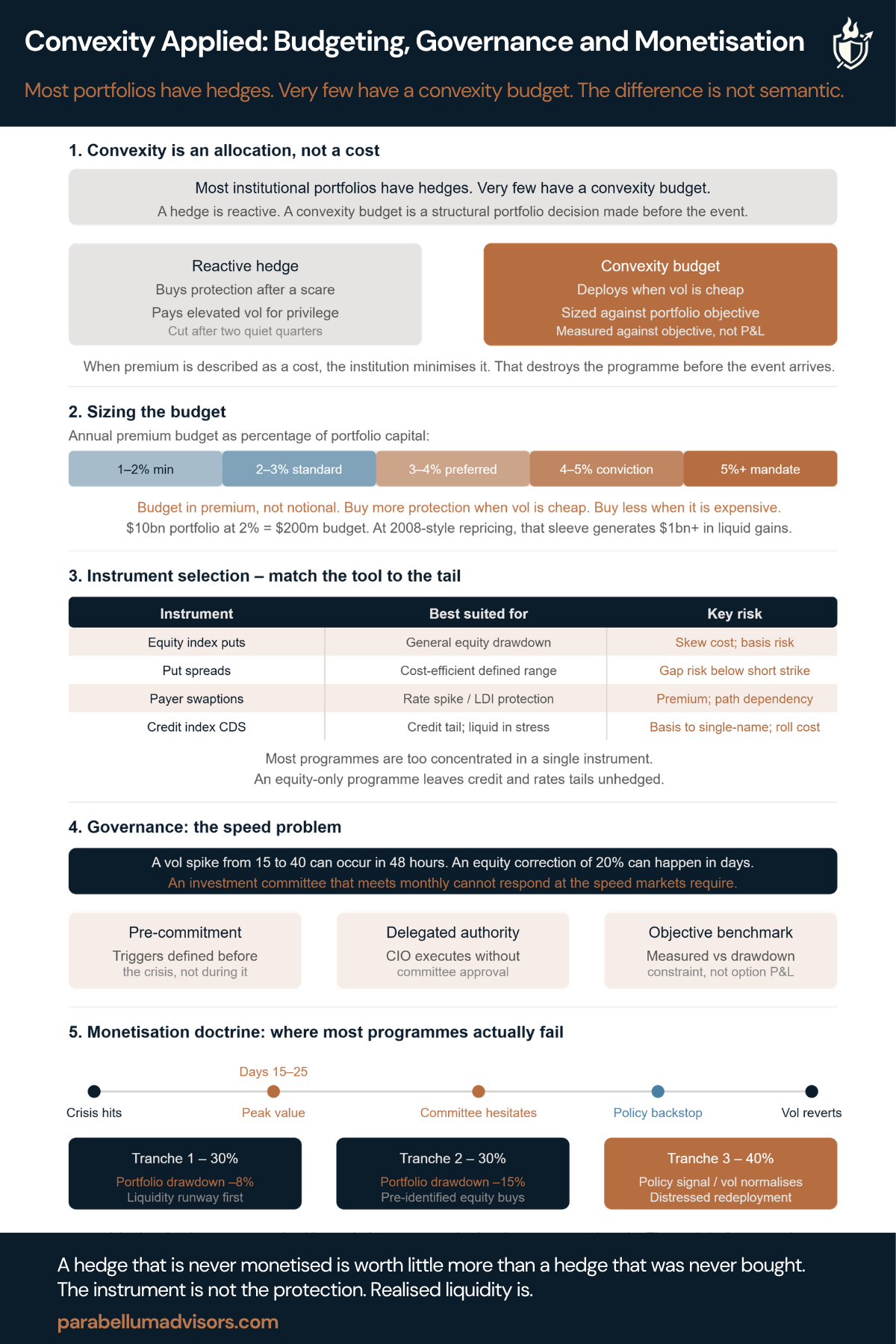

Convexity budgeting. Most portfolios have hedges. Very few have a convexity budget. The difference is not semantic.

A hedge offsets a specific risk. A convexity budget is a deliberate portfolio allocation designed to reshape the distribution of outcomes.

One is reactive. The other is strategic.

Institutions that hedge reactively tend to buy protection after markets have already fallen, implied volatility has repriced, and protection has become expensive.

Institutions with a convexity budget behave differently. They allocate capital to protection before it is needed, size it against a portfolio objective, and judge success against that objective rather than the premium paid in any given year.

Five things every CIO and investment committee should understand.

1. Convexity is an allocation, not a cost

Treat option premium as a cost and the instinct is to minimise it. Smaller notionals. Shorter maturities. Cheaper structures.

Treat convexity as a portfolio allocation and the conversation changes. The objective is no longer to minimise premium. It is to improve portfolio resilience.

2. Size the budget against the objective

Start with the portfolio, not the instrument. What drawdown is acceptable?

What event is the programme designed to defend against?

Budget premium rather than notional. That naturally buys more protection when volatility is cheap and less when it is expensive.

3. Match the instrument to the tail

A single instrument rarely protects every scenario.

Equity puts help in equity sell-offs, payer swaptions protect against rate shocks, credit index CDS protects against credit stress.

A diversified convexity programme should reflect the risks embedded in the portfolio, not simply the most familiar derivative.

4. Governance determines success

Markets move faster than investment committees.A well-designed programme can still fail if every monetisation decision requires a committee meeting.

Pre-committed decision rules and delegated authority are often more valuable than a more sophisticated hedge.

5. Monetisation is where programmes succeed or fail

Buying protection is only half the job. When convexity creates value during a crisis, that value needs to be converted into liquidity while it still exists. Waiting for certainty usually means waiting until volatility has already normalised.

A hedge that is never monetised is worth little more than a hedge that was never bought.

The institutions that build successful convexity programmes are rarely those with the most sophisticated instruments. They are the ones with the clearest objectives, disciplined governance and a pre-committed plan for acting when markets move.

For investment committees reviewing tail-risk protection: do you have a convexity budget, or simply a collection of hedges?