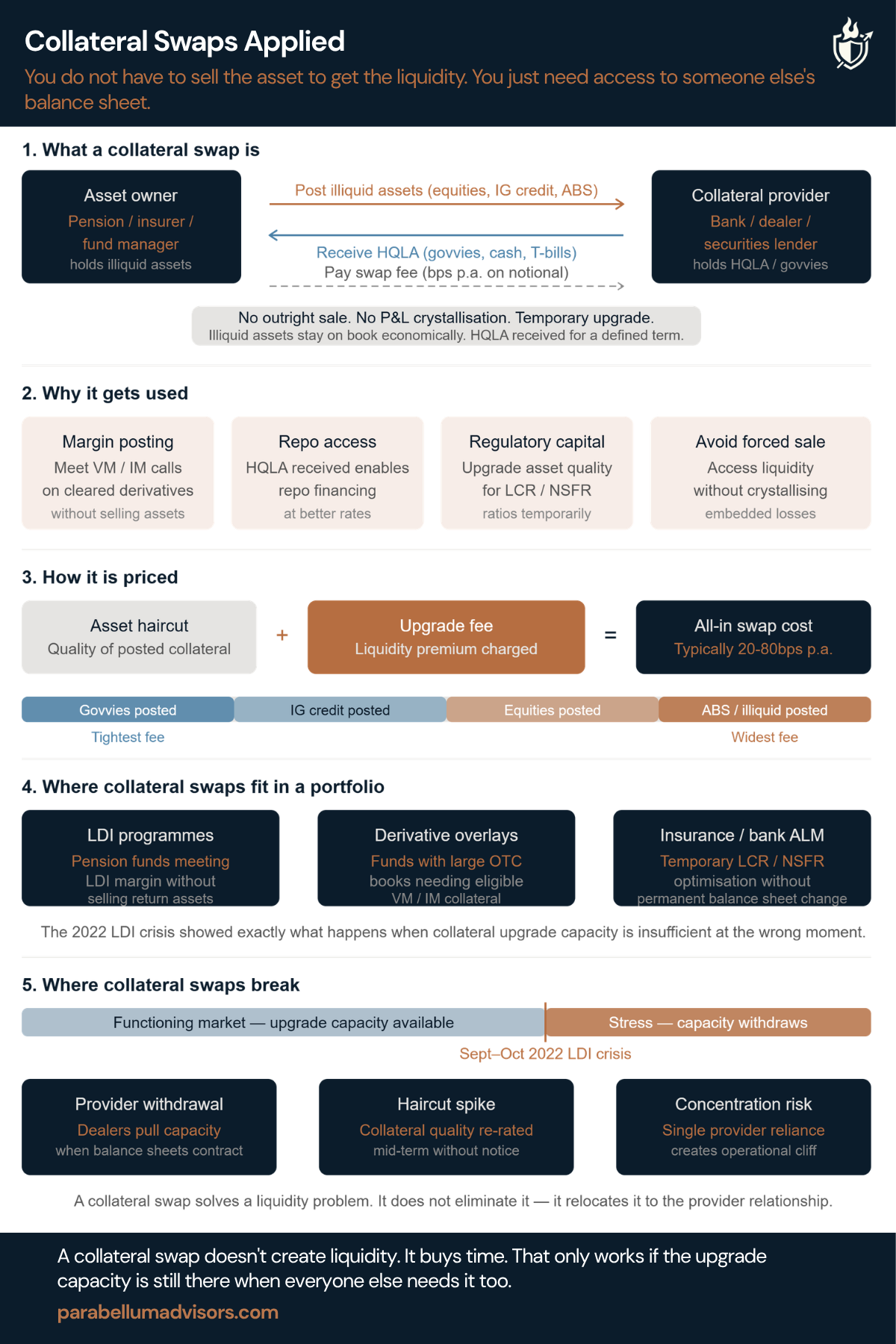

You do not have to sell the asset to raise liquidity. You just need access to someone else’s balance sheet.

A collateral swap allows an investor to temporarily exchange lower-quality or less liquid assets for government bonds or other high-quality collateral.

The underlying assets stay on the balance sheet. Nothing is sold. No gains or losses are crystallised.

That is why collateral swaps are so useful. It is also why they are often misunderstood.

A collateral swap does not create liquidity. It upgrades collateral so the portfolio can continue operating without selling assets at the wrong time.

Five things institutional investors and treasury teams should understand.

1. What a collateral swap actually is

An asset owner temporarily exchanges assets that cannot readily be used for margin with assets that can.

Government bonds, Treasury bills or cash are received for an agreed period in exchange for equities, credit or other less liquid holdings.

At maturity, the assets are returned to their original owners. Economically, nothing has been sold. Only the quality of the collateral has changed.

2. Why they are used

The most common reason is to meet margin requirements without selling long-term investments.

Instead of liquidating assets to obtain eligible collateral, a fund temporarily upgrades its collateral and continues to hold its investment portfolio.

The instrument solves a funding problem without forcing an investment decision.

3. The economics are straightforward

The provider charges a fee for lending higher-quality collateral.

The lower the quality or liquidity of the assets being posted, the higher that fee becomes.

It is an ongoing funding cost, not simply an emergency expense, and should be recognised as part of the economics of any derivatives programme.

4. Where they work well

Collateral swaps play an important role in derivative overlays, LDI portfolios and other strategies where margin requirements can change rapidly.

They reduce the need to hold large cash balances while preserving access to eligible collateral when markets are functioning normally.

5. Where programmes fail

The 2022 UK LDI crisis demonstrated the real risk. The instrument itself worked exactly as intended. What disappeared was dealer balance sheet capacity.

Some facilities proved too small. Others became slower to access. Some providers faced their own constraints just as clients needed collateral most.

The lesson was not that collateral swaps fail. It was that upgrade capacity is finite and should never be assumed to exist when every market participant needs it simultaneously.

Collateral swaps remain one of the most effective tools for managing liquidity within a derivatives programme.

The real risk is not the instrument. It is assuming someone else’s balance sheet will always be available when your own portfolio needs it most.