Counterparty risk. A profitable hedge is worthless if nobody is left to pay you.

When people talk about derivatives, the conversation almost always revolves around market risk. Where will interest rates go? What happens if the currency moves? How much could equities fall?

Those questions matter.

But there is another risk that receives far less attention. What happens when the hedge works exactly as planned, the position is substantially in the money, and the institution on the other side is under severe stress?

That is counterparty risk. Unlike market risk, it only becomes a problem when you are supposed to be winning.

Five observations from managing institutional derivative portfolios.

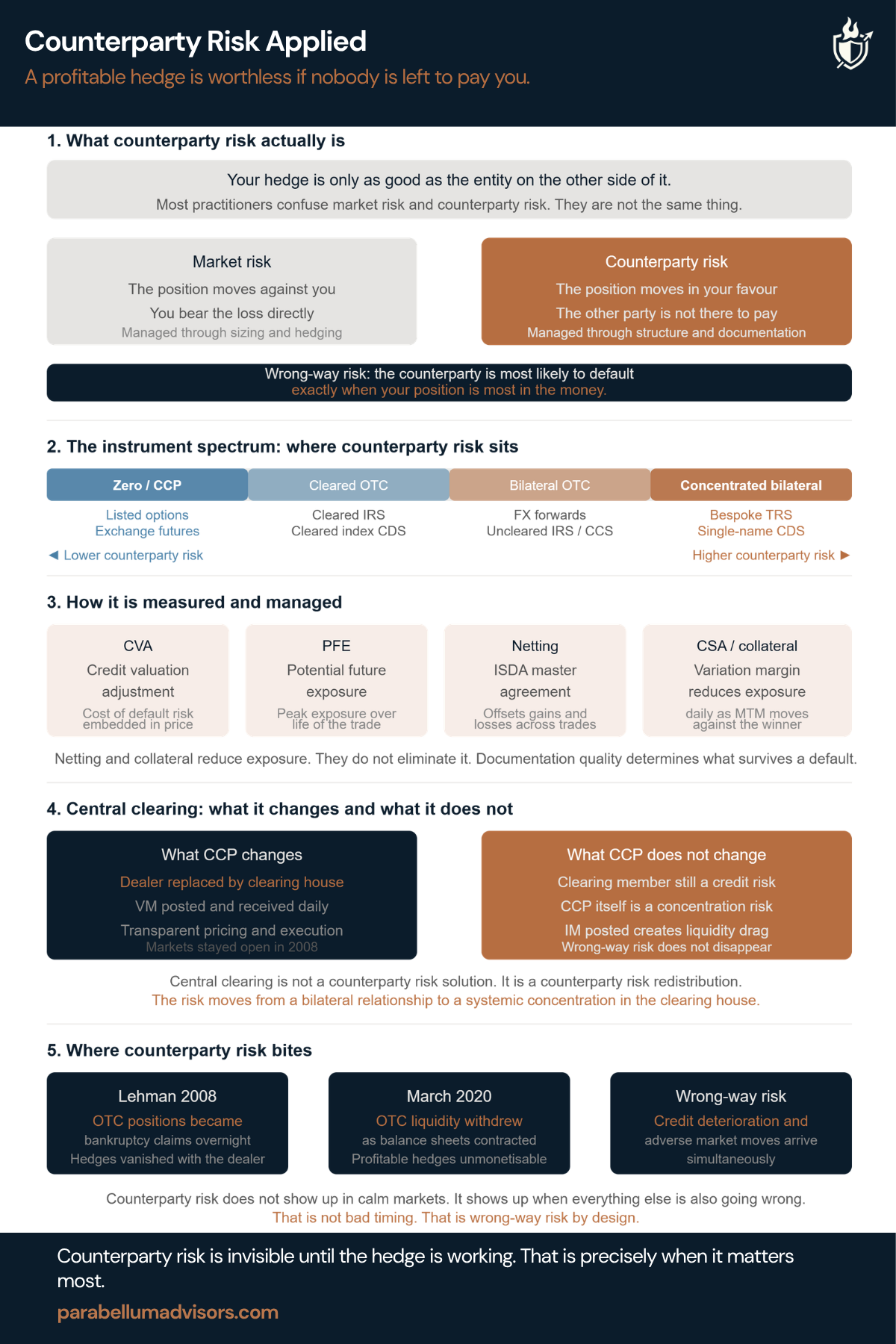

1. Market risk and counterparty risk are different problems.

A hedge can perform perfectly from a market perspective and still fail economically if the counterparty cannot perform. In stressed markets those two risks often become connected. The same conditions that make your hedge valuable may also place pressure on the institution expected to pay you.

2. Not every derivative carries the same counterparty exposure.

Listed futures and options rely on a clearing house. Cleared swaps significantly reduce bilateral exposure. Uncleared OTC trades, bespoke structures and long-dated bilateral agreements depend far more heavily on the credit quality of the institution on the other side, together with the strength of the ISDA and collateral arrangements supporting them.

3. Documentation matters as much as pricing.

ISDA agreements, collateral terms, netting provisions and margin arrangements rarely receive much attention when markets are calm. During periods of stress they often become more important than the economics of the trade itself. A well-collateralised position behaves very differently from one relying on unsecured exposure.

4. Central clearing improves the picture but does not eliminate the risk.

The reforms after 2008 materially strengthened the system, but they did not remove counterparty risk altogether. They redistributed it. Clearing members, collateral requirements and liquidity demands still need to be managed, particularly when volatility increases sharply.

5. The biggest mistakes are governance failures.

Most institutions spend considerable time deciding which dealer wins a transaction. Far fewer regularly review aggregate exposure across counterparties, stress-test dealer concentration or consider what happens if liquidity disappears when they need to monetise a profitable hedge.

That is usually where the weakness sits.

Counterparty risk is rarely visible in normal markets. It becomes obvious when liquidity contracts, balance sheets come under pressure and the hedge is doing exactly what it was designed to do.

By then it is far too late to start reading the ISDA.