Bond forwards. Most institutions extend duration with swaps. Sometimes the better answer is to lock the bond instead.

When institutions need more duration, the default answer is usually an interest rate swap. It is liquid, familiar and efficient. Pay fixed, receive floating, and the portfolio’s interest-rate sensitivity increases immediately.

For many portfolios, that is exactly the right solution. But if the objective is to own a specific long-dated bond at a known yield in the future, a swap introduces something that the underlying liabilities often do not have: a floating-rate leg that resets throughout the life of the trade.

A bond forward approaches the problem differently.

Five things insurance ALM teams, pension funds and fixed income investors should understand about bond forwards.

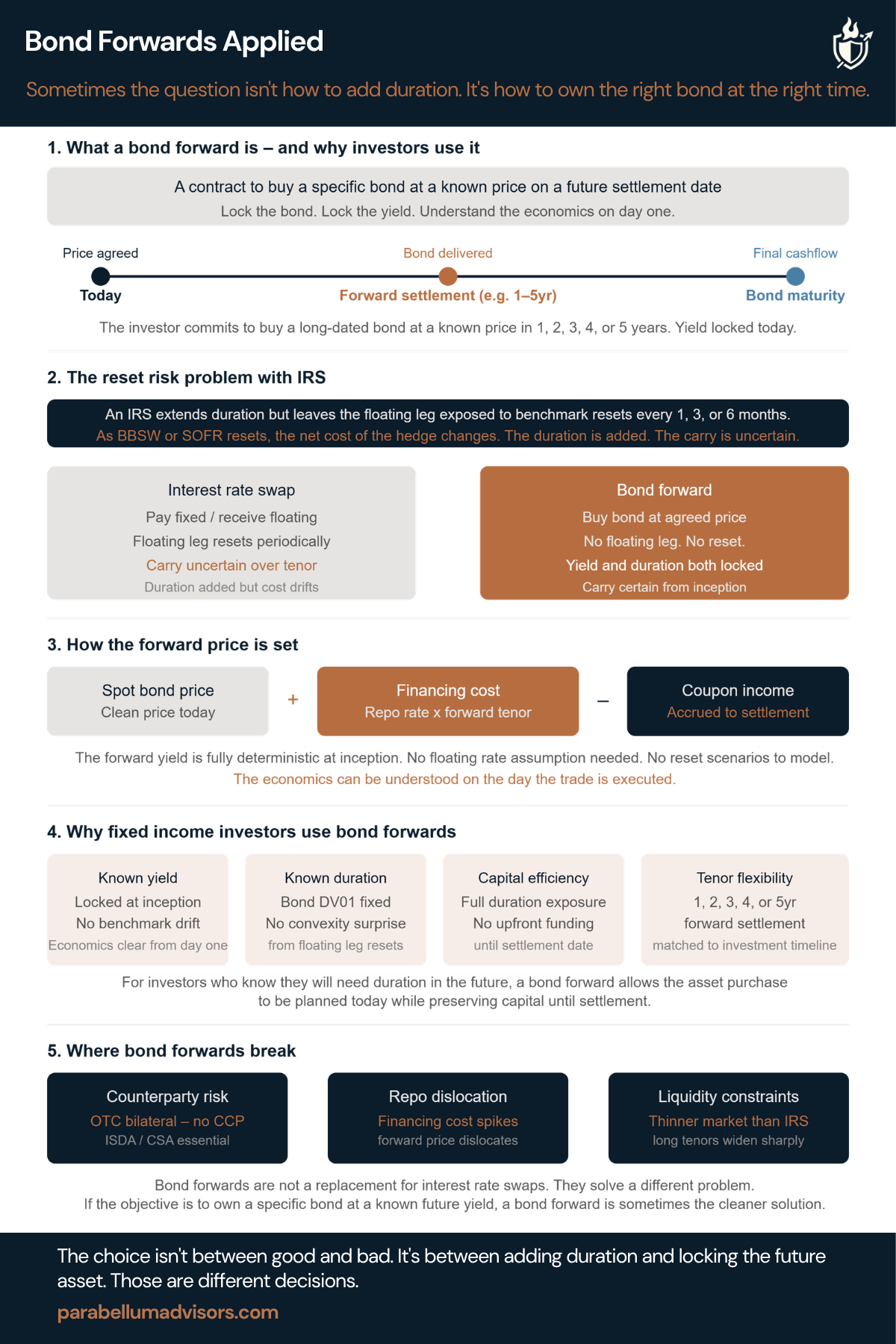

1. What a bond forward actually is

A bond forward is simply an agreement to buy a specific bond at a future date for a price agreed today. The purchase happens later, but the economics are largely locked from the outset. The investor knows which bond they will receive, the settlement date and the yield they are effectively securing.

2. Why some investors prefer them

An interest rate swap changes duration without owning the bond. A bond forward locks the future purchase of the actual asset. For insurers matching long-dated liabilities, that distinction can matter. The asset ultimately sitting on the balance sheet is the same asset that was planned years earlier.

3. The economics are easier to understand than many expect

The forward price is based on today’s bond price, adjusted for financing and coupon income over the forward period. There is no floating benchmark resetting every few months and no uncertainty around future swap carry. The economics can be understood on the day the trade is executed.

4. Where they fit

Bond forwards work well when an institution knows it will need duration in the future but does not want to fund the bond purchase today. They allow the future asset purchase to be planned while preserving capital until settlement. For insurers building long-dated portfolios over several years, they can provide a more direct link between today’s hedging decision and tomorrow’s asset allocation.

5. Where they can disappoint

Bond forwards remain bilateral OTC contracts. Liquidity is generally lower than the swap market, particularly at longer maturities, and pricing depends on dealer appetite. Counterparty exposure and documentation therefore matter just as much as the pricing itself. Like many derivative structures, the instrument is usually straightforward. The execution framework is where problems emerge.

Bond forwards are not a replacement for interest rate swaps. They solve a different problem.

If the objective is simply to add duration, a swap is often the obvious choice. If the objective is to own a specific bond at a known future yield, a bond forward is sometimes the cleaner solution.