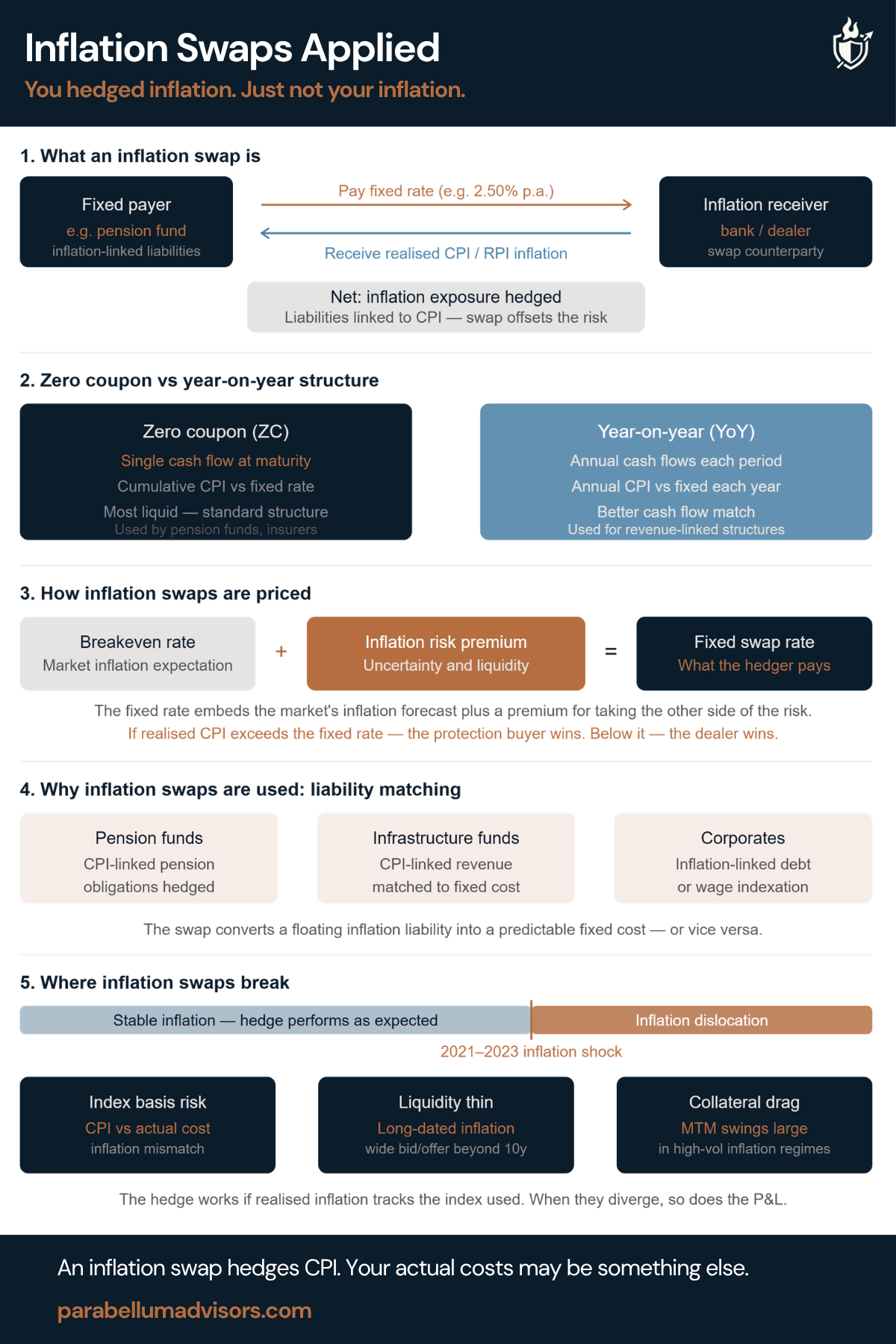

You hedged inflation. Just not your inflation.

An inflation swap converts a floating inflation liability into a predictable fixed cost. For pension funds with CPI-linked obligations, infrastructure funds with inflation-linked revenue, and corporates with indexed debt, the instrument does what it says.

The risk is not in the swap. It is in assuming the inflation index tracks your actual cost base closely enough to matter.

Five things to understand about inflation swaps.

1. What it actually is

A bilateral agreement to exchange a fixed rate for realised inflation over a defined tenor. The fixed payer pays an agreed rate and receives the actual CPI or RPI print. No principal changes hands. The net payment reflects the difference between the fixed rate and the inflation index.

2. Zero coupon vs year-on-year

The zero-coupon structure is the market standard: a single net cash flow at maturity reflecting cumulative realised inflation against the fixed rate. It is the most liquid structure and is widely used for long-dated liability management.

The year-on-year structure settles annually. It is less liquid, but often a better economic fit for infrastructure assets and revenue-linked businesses with annual CPI reset mechanisms.

3. How it is priced

The fixed rate reflects the market’s breakeven inflation expectation plus an inflation risk premium. It is the market’s clearing price for transferring inflation uncertainty, not a forecast.

If realised inflation averages above the fixed rate, the fixed payer receives net payments. If it averages below, they make net payments.

4. Liability matching

Pension funds use inflation swaps to convert CPI-linked obligations into predictable fixed costs.

Infrastructure investors use them to align CPI-linked revenue with fixed financing costs.

Corporates with indexed debt or wage indexation use them to convert uncertain future costs into a budgetable fixed rate.

5. Where it breaks

Index basis risk is the primary failure mode. CPI measures a standardised basket of consumer prices. Your actual exposure may be driven by wages, construction costs, energy or imported materials, none of which necessarily move with the index. During 2021-2023, headline CPI rose sharply, but the drivers differed materially across sectors. The instrument can work while the exposure does not.

Liquidity is the second risk. Long-dated inflation swaps beyond ten years remain relatively illiquid in most markets outside the US and UK. In Australia, liquidity falls away materially beyond seven years.

Collateral drag is the third. Large mark-to-market movements can generate significant margin calls for investors without dedicated collateral infrastructure.

Inflation swaps are the right instrument for genuine inflation liability mismatches.

The question is not whether the swap hedges CPI. It is whether CPI is actually the inflation you need to hedge.