Your hedge worked. You still made nothing. Here’s why.

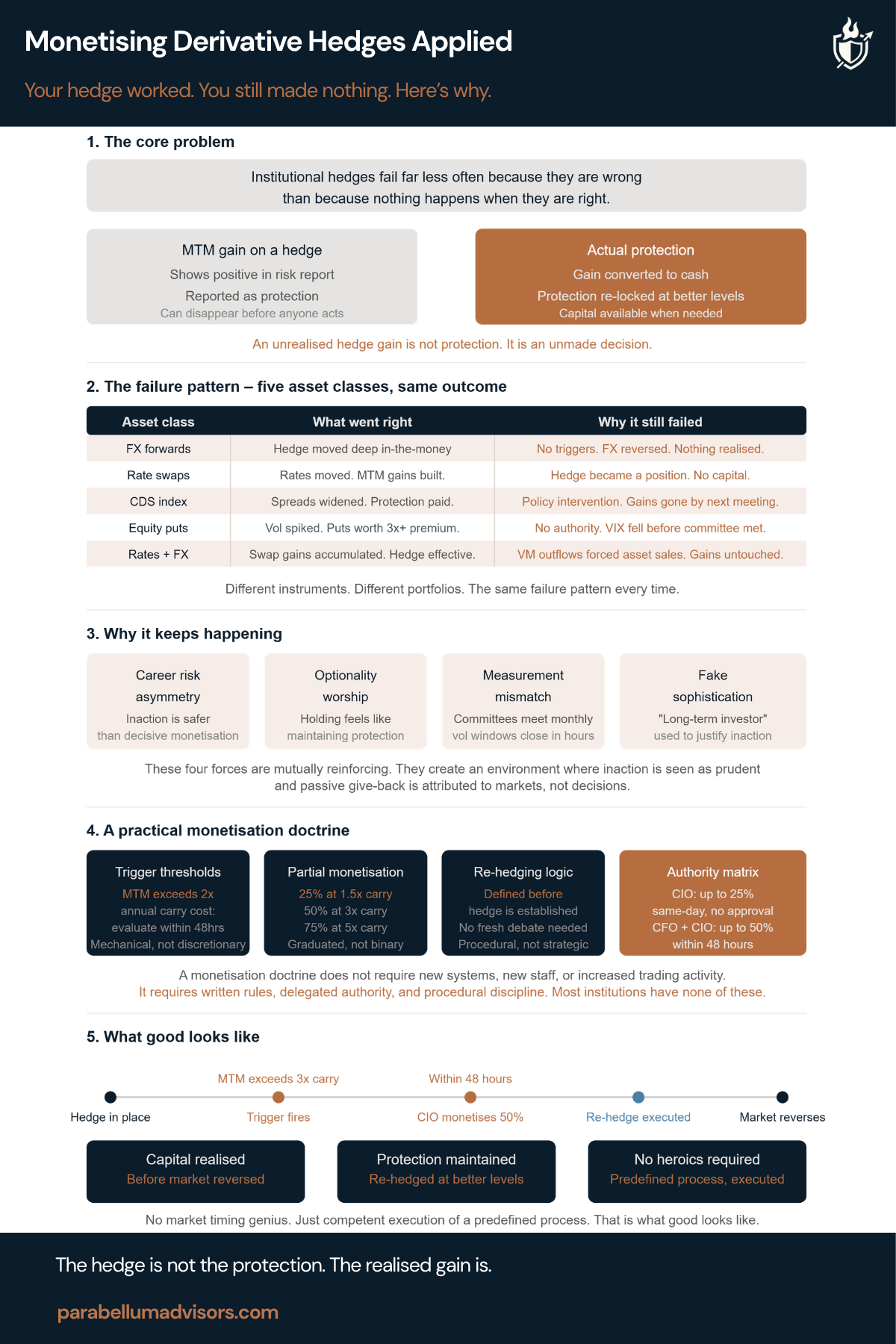

Institutional hedges fail far less often because they are wrong than because nothing happens when they are right.

Across FX, interest rates, credit, equity and volatility, portfolios routinely build hedges that perform exactly as intended. The mark-to-market improves. Risk reports look reassuring. Investment committees gain confidence that protection is working.

Then markets recover. The gains disappear. Nothing was ever realised.

The problem is rarely the hedge itself. It is the absence of a monetisation framework.

Five things every CIO, treasury team and investment committee should understand.

1. A MTM gain is not protection

One of the most common misconceptions in risk management is that an unrealised hedge gain somehow represents completed protection. It doesn’t.

Until that gain is realised, re-locked at better market levels or used to strengthen the portfolio, it remains conditional. Markets reverse. Volatility normalises. Carry erodes value. What looked like protection becomes another opportunity missed.

2. The failure pattern is remarkably consistent

The instrument changes. The outcome rarely does.

FX forwards move materially in-the-money before exchange rates reverse. Interest rate swaps become increasingly valuable before yields retrace. CDS positions widen dramatically before policy intervention compresses spreads. Equity puts triple in value during a market panic before volatility collapses.

Different markets. Different instruments. The same result. The hedge worked, but nobody had agreed what to do next.

3. Governance usually matters more than market timing

Most institutions don’t lose hedge gains because they lack technical capability. They lose them because decisions move more slowly than markets.

Committees meet monthly. Markets reprice in days. The CIO knows action is justified but lacks delegated authority. The committee wants more certainty. By the time certainty arrives, the opportunity has gone.

The issue isn’t forecasting. It’s governance.

4. Monetisation should be designed before the hedge

Every hedge should have a written monetisation framework before the trade is executed. When should gains trigger review? How much can be realised? How will the hedge be rebuilt? Who has authority to act?

Those decisions should never be made during a crisis. By then, markets are moving faster than governance.

5. Good monetisation is surprisingly boring

The best programmes rarely rely on brilliant market calls. A threshold is reached. Part of the gain is realised. The hedge is resized or re-established. Liquidity is created.

The portfolio remains protected. No heroics. No perfect market timing. Just disciplined execution against a framework agreed well before markets became stressed.

Hedges that cannot be monetised when they work do not fully protect a portfolio. They simply postpone the decision a crisis creates.