The premium wasn’t the biggest cost. The basis was.

A single-name CDS gives protection on one borrower. An index CDS gives protection on a standardised basket: 25, 100, or 125 names depending on the index. One trade, broad credit exposure.

That simplicity is the appeal. The complexity is in the carry, the basis, and what happens when the hedge actually needs to perform.

Five things to understand about index CDS.

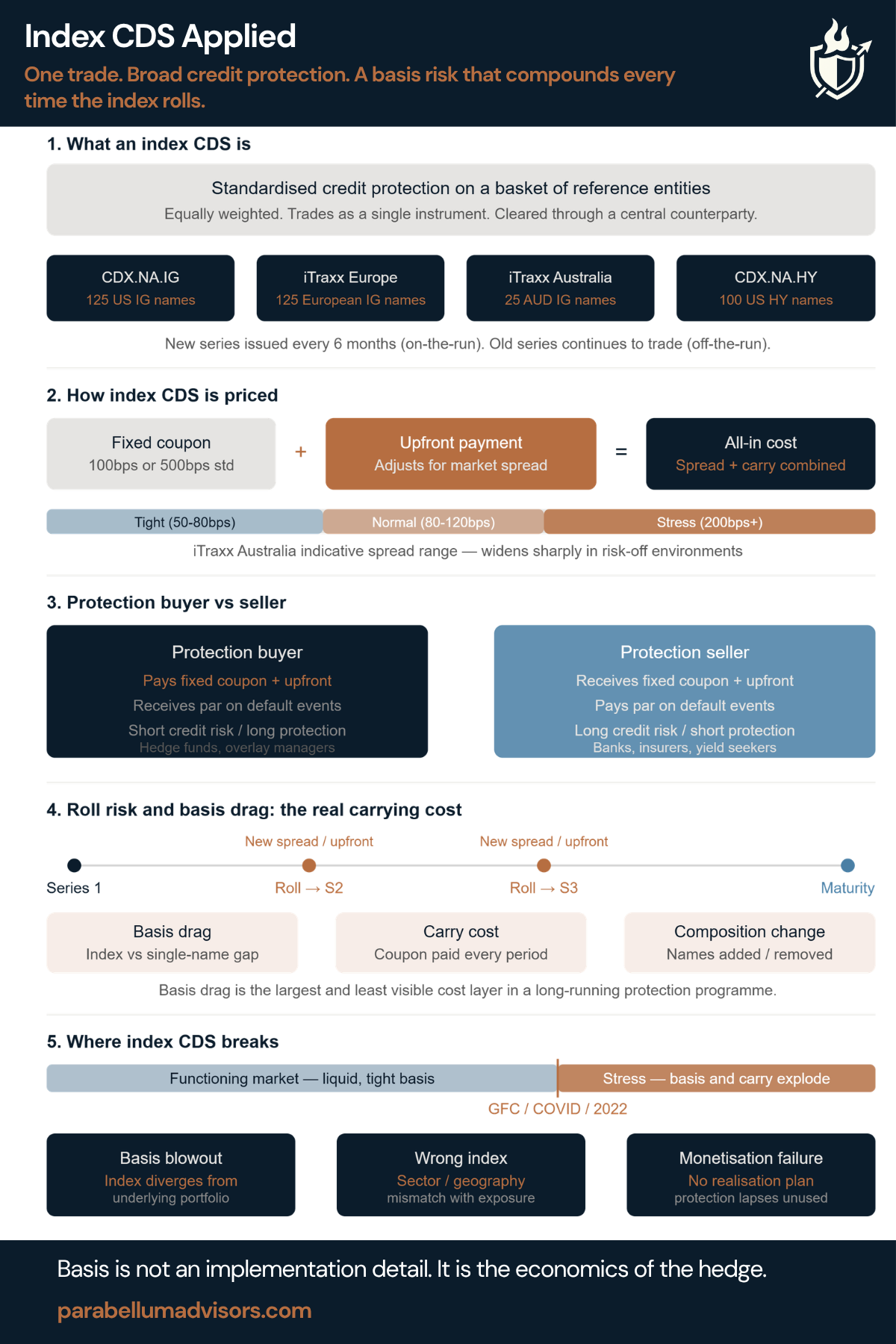

1. What an Index CDS is

A standardised contract providing credit protection on an equally weighted basket of reference entities. If a name defaults, the protection buyer receives par minus recovery on that name’s notional. The index continues with the remaining names. Major series include CDX.NA.IG, iTraxx Europe, iTraxx Australia and CDX.NA.HY. New series are issued every six months. Old series continue trading off-the-run.

2. How it is priced

Index CDS uses a fixed coupon, typically 100bps for investment grade and 500bps for high yield, with an upfront payment reflecting where market spread sits versus coupon. If the index trades below coupon, the buyer receives upfront. If it trades above coupon, the buyer pays upfront. The all-in cost is expressed as a running spread equivalent.

3. Protection buyer vs seller

The buyer pays coupon and upfront, receives par on default events, and benefits when spreads widen or defaults occur. The seller receives coupon and upfront, pays out on defaults, and is synthetically long the basket. Buyers are typically hedge funds, overlay managers and institutional hedgers. Sellers include banks, insurers and yield-seeking funds.

4. Roll risk and basis drag

Index CDS series roll every six months. Each roll is a new trade at current spreads with a new upfront. Basis drag, the gap between the index spread and the actual credit risk of the portfolio, accumulates quietly across every roll. For a private credit or infrastructure fund using iTraxx as a macro hedge, the index and portfolio will never match perfectly. In stress, that mismatch can become material.

5. Where it breaks

Basis blowout is the primary failure mode. The index widens but the specific names in your portfolio do not, or vice versa. In 2020, investment grade indices widened sharply while some private credit portfolios with stronger covenants held. The hedge performed, but it overshot.

The second failure mode is monetisation. Buying protection, holding it through spread widening, then rolling rather than realising the gain. A protection programme without a monetisation framework is not a hedge. It is a carry cost with an uncertain payoff.

Index CDS is the right instrument for managing broad credit risk at portfolio level. The basis to any specific underlying will never be zero. The question is whether carry cost and basis risk are priced into the mandate upfront or discovered after the fact.