You removed the headline FX risk. You kept the basis, the MTM, and the collateral call nobody modelled.

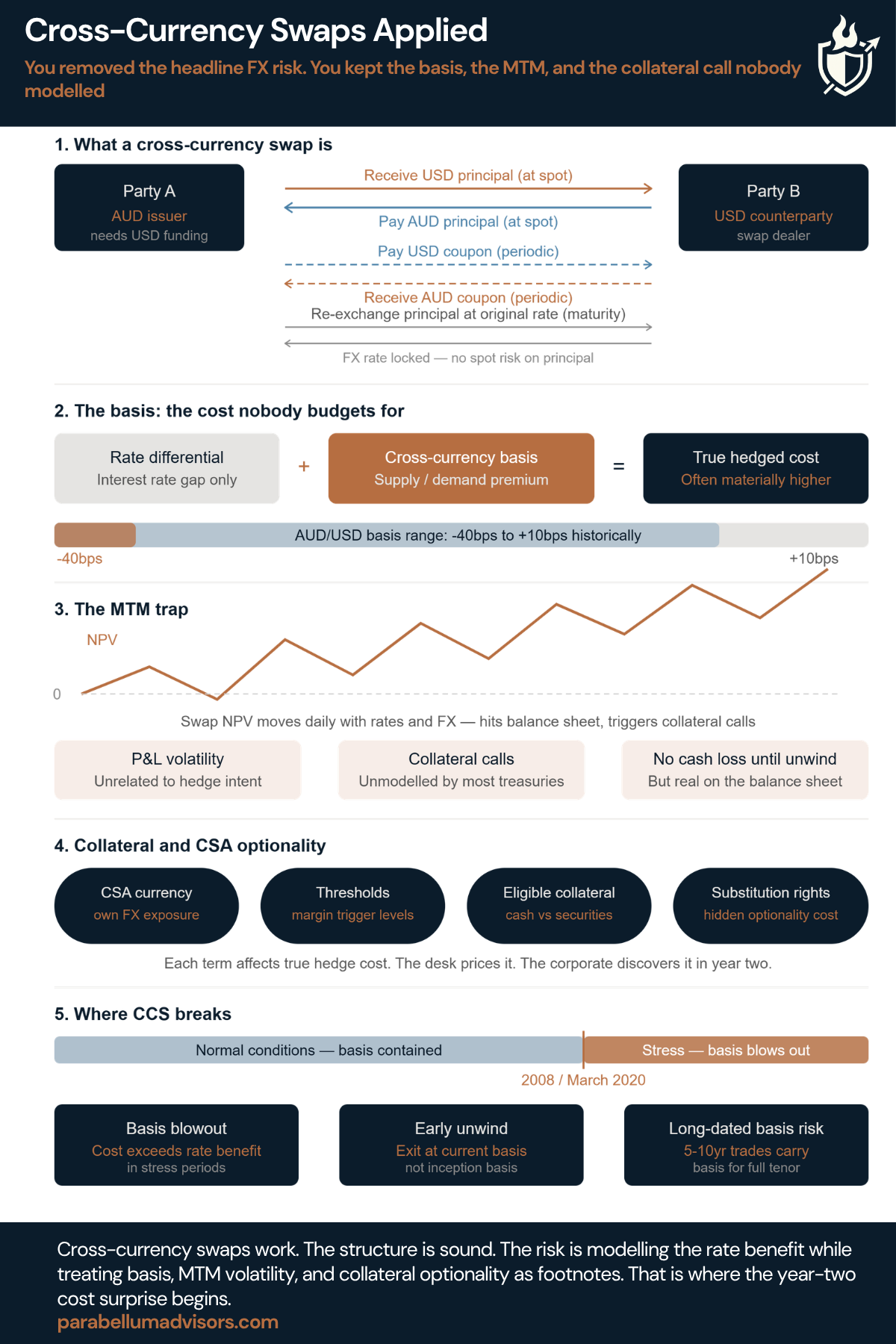

A cross-currency swap lets you borrow in one currency and service the debt in another. The coupon payments swap. The principal swaps back at maturity at the original rate. On paper, the FX risk disappears.

What does not disappear is the basis. That is where many get surprised, not at inception, but 2 years in when the all-in cost looks nothing like the term sheet.

Five things you need to understand before you enter a cross-currency swap.

1. What a cross-currency swap actually is

Two parties exchange principal in different currencies at inception. Throughout the life of the trade, they exchange coupon payments in those respective currencies. At maturity, the principal is re-exchanged at the original spot rate. The FX exposure on the underlying bond or loan is neutralised. What changes hands at every coupon date is the interest differential, and the basis layered on top of it.

2. The basis: the cost gets under-modelled

Cross-currency basis is a spread on top of the interest rate differential. It reflects supply and demand dynamics in the swap market, not interest rate fundamentals. It is real, it moves, and it is almost never modelled properly at the start of a programme. AUD/USD basis has historically traded between -40bps and +10bps. The rate on the term sheet is not the all-in cost. It is the starting point.

3. The MTM trap

Cross-currency swaps are marked to market daily. As rates and FX move, the NPV shifts. For a corporate or fund with liability-driven mandates, this creates P&L volatility that has nothing to do with the underlying exposure being hedged. It is not a cash loss until the trade is unwound, but it hits the balance sheet, can trigger collateral calls, and will eventually appear in front of an audit committee that was not briefed on it at inception.

4. Collateral and CSA optionality

If the CCS is collateralised under a CSA, variation margin moves with the MTM. The CSA currency, threshold amounts, and eligible collateral types all affect the true economic cost of the hedge in ways that are difficult to price upfront. If you are posting collateral in a currency that is not your functional currency, you have introduced a secondary FX exposure.

5. Where CCS breaks

Basis blowout during stress is the primary failure mode. In 2008 and March 2020, cross-currency basis moved to levels that made the economic cost of the hedge materially worse than the rate differential benefit it was designed to capture. For long-dated structures running five to ten years, you are carrying meaningful basis risk for the full tenor.

Cross-currency swaps are the right instrument for genuine currency-liability mismatches. The problems come from treating basis, MTM volatility, and CSA optionality as footnotes rather than rather than as core components of the cost analysis.