By Mike Duncan | January 2026

When concentration risk meets real-world constraints on selling, timing, and signalling.

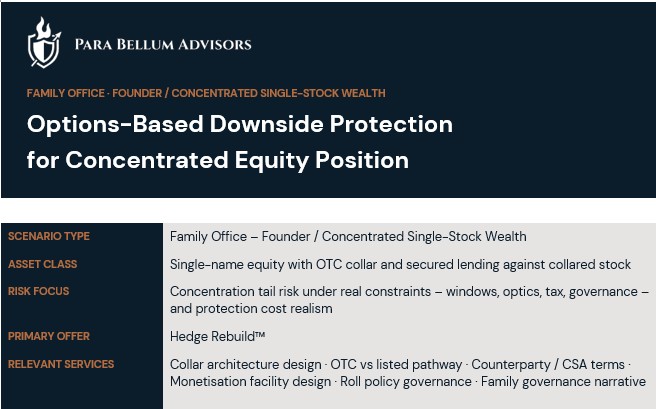

Sector: Family Office – Founder / Concentrated Wealth

Asset Class: Single-Name Public Equity with Derivative Overlay

Situation Type: Highly concentrated equity exposure with constraints on selling, signalling, tax, and timing

Primary Issue: Tail risk concentration under real-world constraints, where selling is limited and ad-hoc hedging becomes economically and operationally unsustainable

The Situation

A family office holds a dominant position in a single publicly listed equity following an IPO or liquidity event.

The exposure represents a material proportion of family net worth. Diversification is acknowledged as desirable, but execution is constrained by disclosure optics, tax considerations, trading windows, and founder psychology.

On paper, the risk is understood. In practice, the ability to act during stress is limited.

The absence of a structured protection framework leaves the family fully exposed to a sharp drawdown at precisely the moment when selling may be impractical or impossible.

Why This Scenario Is Common

-

Concentration is initially viewed as temporary

-

Diversification is deferred to avoid signalling or tax leakage

-

Hedging is postponed rather than designed

-

Liquidity windows narrow as volatility rises

-

No pre-committed response exists for sharp drawdowns

-

Governance assumes decisions can be made “when needed”

The exposure persists. The optionality to act does not.

Why It Matters

When a large single-name drawdown occurs:

-

Selling into weakness creates signalling and tax damage

-

Trading windows often close during peak volatility

-

Ad-hoc hedging becomes expensive or infeasible

-

Governance decisions become reactive and stress-driven

The risk is not volatility. It is being forced to decide under pressure with no viable options.

How This Is Typically Addressed

-

Accepting concentration risk until diversification feels “easier”

-

Considering outright put protection without a sustainable framework

-

Executing one-off hedges with no roll discipline

-

Avoiding OTC structures due to perceived complexity

These approaches delay action without restoring control.

Primary Engagement Route

Primary Offer: Hedge Rebuild™ – Concentrated Equity Protection Reset

Design of a maintainable options-based protection framework, addressing structure architecture, OTC execution, collateral mechanics, and roll governance – without introducing tactical trading risk.

Secondary / Bespoke:

Monetisation facility design, CSA and counterparty structuring, 10b5-1 coordination support, and family-grade reporting.

Full structural narrative shared selectively on request.

Illustrative scenario for discussion purposes only. Not a transaction summary or client-specific case study.